Answer:

Cost of common from reinvested earnings = 10.44 %

so correct option is c. 10.44%

Explanation:

given data

D1 = $0.67

Po = $27.50

g = 8.00%

to find out

cost of common from reinvested earnings based on the DCF approach

solution

we get here Cost of common from reinvested earnings that is express a s

Cost of common from reinvested earnings =  + g ............1

+ g ............1

put here value we get

Cost of common from reinvested earnings =  + 8%

+ 8%

Cost of common from reinvested earnings = 10.44 %

so correct option is c. 10.44%

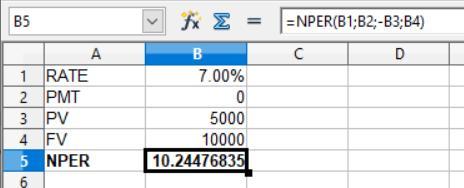

Answer:

10.24 years

Explanation:

For this question we use the NPER function that is shown on the attachment. Kindly find it below:

Data provided in the question

Present value = $5,000

Future value = $10,000

Rate of interest = 7%

PMT = $0

The formula is shown below:

= NPER(Rate;PMT;-PV;FV;type)

The present value come in negative

So, after solving this, the answer would be 10.24 years

Answer:

Following are the two reasons for why someone looking at a career in the Energy cluster might want to focus on new technology, such as energy-efficient products or sustainable energy;

- Energy efficient technologies are now found in most energy conversion chains. For example from production of primary energy resources to power generations.

- Technology helps to improve the conversion of energy better. For example the conversion of wasted energy released in the form of heat.

Following are the two examples of careers that may work with these new energy technologies;

- A career in renewable energies which use high end technologies.

- A career in generating energy from natural resources like the solar energy from the sun.

Answer:

communication costs

Explanation:

Communication is critical for the success of a business. If the communication cost is high, then communication can become a hindrance to the success of business success. The costs associated with communication include fixed telephone, mobile phones cost, and internet access. Travel and venue cost that facilitates face-face meeting also adds to communication costs.

Businesses are embracing modern technology to cut down on their communication cost. Technology has increased the flow of internal and external communication. Magnet Dot is likely to grow as a business as customers can order for products over the internet.

<span>A bank is legally required to hold a fraction of its deposits as required reserves. These regulations are a requirement and set by most banks around the world. They set minimum amounts that must be held all the type to serve as a reserve in case of an </span>emergency.