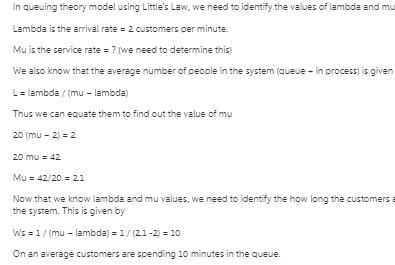

Answer:

On an average customers are spending 10 minutes in the queue.

Explanation:

Please see attachment

Answer:

Explanation:

a. The computation of the ending inventory is shown below:

Inventory Quantity Cost NRV LCM Total inventory

(1) (2) (1 × 2)

Unit A 14 $38 $40 $38 $532

Unit B 22 $42 $39 $39 $858

Unit C 16 $27 $31 $27 $432

Unit D 19 $18 $17 $17 $323

Total $2,145

And total cost = Unit A × cost + Unit A × cost + Unit A × cost + Unit A × cost

= 14 × $38 + 22 × $42 + 16 × $27 + 19 × $18

= $532 + $924 + $432 + $342

= $2,230

b. The journal entry is shown below:

Income summary A/c Dr $85 ($2,230 - $2,145)

To Inventory A/c $85

(Being inventory is adjusted)

<span>Street Survivors was the fifth studio album of the rock group Lynyrd Skynyrd, recorded in 1977. In October of that year, a small plain carrying members of the band as well as managers and support personell, crashed near Gillsberg, Mississippi. Lead Vocalist Ronnie Van Zant, guitarist Steve Gaines, and backup vocalist Cassie Gaines were among the six killed.</span>