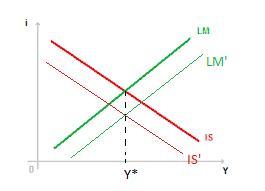

Answer:

Have an expansionary monetary policy (shift LM curve to the right)

Explanation:

See the graph attached. If the IS curve shifts to the left, there will be a new IS curve- The IS'. If the Fed wants to keep the output level (Y) unchanged, then it has to shift the LM curve to the right, to LM', so that the Y point (output level) in which the IS matches the LM stays the same (Y*).

Shifting the LM curve to the right, it means to have an expansionary monetary policy, which means to expand the quantity of money in the economy. This is done, for example, by decreasing the discount rate or reducing the reserve ratio.

Answer:

Option C, a municipal securities broker's broker.

Explanation:

Option “C” is correct because these broker acts on the behalf of the client and perform all the transactions without exhibiting their client’s details in the market. Moreover, the broker maintains the bonds or securities and it focuses on the profit-making aspects. Finally, the broker receives the commission for their service and the client receives the profit or rate of return from the securities.

1620

900 times 8%, or 0.08 is 72. So 72 is the interest for 1 year. You multiply that times 10 for ten years of interest and get 720. You add 900 and 720 and you get 1620. Therefore, 1620 is how much you have after 10 years with eight percent interest. Hopefully this helps!

Sally needs to deliver customer sales data to multiple departments in real-time by using customizable reports.

<h3>What do you mean by accounting?</h3>

Accounting is a means of collecting, summarizing, analyzing, and reporting business information in monetary terms.

As sally needs to deliver the customer sales data to multiple departments in real-time, customizable reports can be helpful in this case.

A customizable report is a type of report that is created and metrics and dimensions should be added and it will display in the way.

Therefore, OB is the correct option.

Learn more about accounting here:

brainly.com/question/5399294

#SPJ1

Answer:

The bond portfolio’s Macaulay duration is 5.50

Explanation:

According to the following formula

Portfolio duration = weighted duration = (weight of Bond A*Duration of A) + (weight of Bond B*Duration of B)

= ((10,000/40,000) *5) + ((30,000/40,000) *6) = 5.50