Answer and Explanation:

The journal entries are shown below:

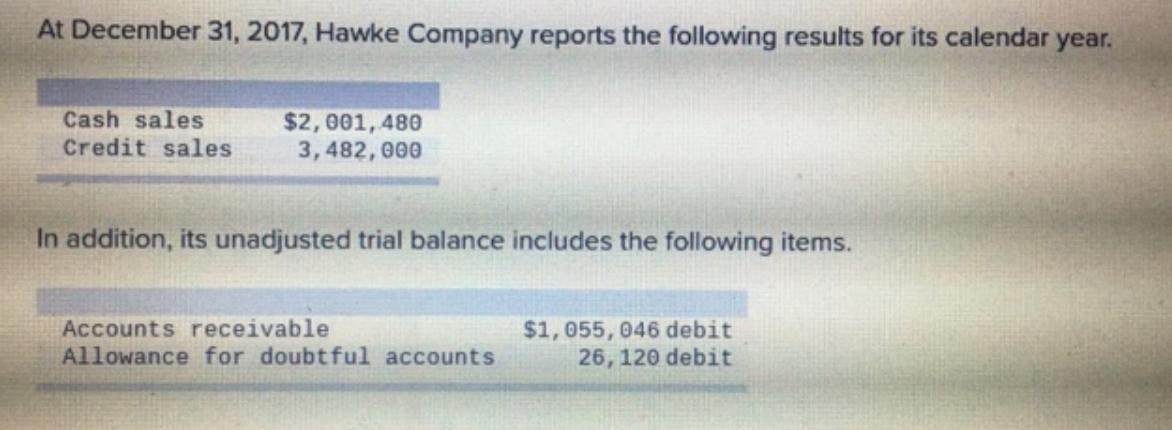

a. Bad debts expense$139,280 ($3,482,000 × 4%)

To Allowance for doubtful accounts $139,280

(Being the bad debt expense is recorded)

For recording this we debited the bad debt expense as it increased the expenses and credited the allowance as it reduced the asset

b. Bad debts expense $109,670 (($2,001,480 + $3,482,000) × 2%)

To Allowance for doubtful accounts $109,670

(Being the bad debt expense is recorded)

For recording this we debited the bad debt expense as it increased the expenses and credited the allowance as it reduced the asset

c. Bad debts expense $99,973.22 (($1,055,046 × 7% + $26,120)

To Allowance for doubtful accounts $99,973.22

(Being the bad debt expense is recorded)

For recording this we debited the bad debt expense as it increased the expenses and credited the allowance as it reduced the asset