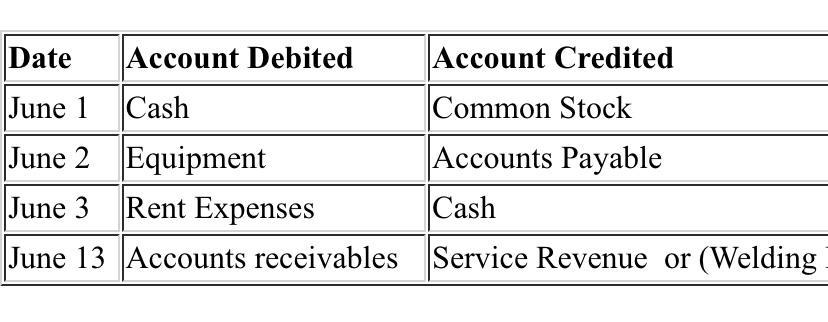

Answer:

Journal Entries:

Dec 31 Bad Debts Expense $4875

Allowances for doubtful accounts $4875

Feb 1 Allowances for doubtful accounts $580

Accounts Receivable - P.Park $580

June 05 Accounts Receivable - P.Park $580

Allowances for doubtful accounts $580

June 05 Cash $580

Accounts Receivable - P.Park $580

Explanation:

On December 31 Chen estimates the potential receivable expected to be not paying to him. Therefore, he write off the receivable from balance sheet using the percentage of sales method of receivable of ($975000 x 0.5% = $4875). On Feb 1 Chen write off P.Park from receivable of $580 as he comes to know he will not pay but on June 5 P.Park pay him $580. First Chen reinstate the receivable afterwards he collect cash from receivable.

Financial records are used for taxes, to show investors, to prove strength of the company in order to get loans. It is vital that financial records are accurate and up to date because of the many people that rely on the data.

Tim should be in governance.

Suzette should be in planning

Answer:

(a) $5,690

(b) $380

Explanation:

Given that,

current assets = $2,090

Net fixed assets = $9,830

Current liabilities = $1710

Long-term debt = $4520

Total assets:

= Current assets + Net fixed assets

= $2,090 + $9,830

= $11,920

Total Liabilities:

= Current Liabilities + Long-term Debt

= $1710 + $4520

= $6,230

(a) Total assets = Total liabilities + Stockholder's equity

$11,920 = $6,230 + Stockholder's equity

$11,920 - $6,230 = Stockholder's equity

$5,690 = Stockholder's equity

(b) Net working capital:

= Current assets - Current liabilities

= $2,090 - $1,710

= $380