Answer:

A. $153,000

Explanation:

The Journal Entry is shown below:-

Property Dr, $1,173,000

To Treasure stock $1,020,000

To additional paid-in-capital $153,000

The computation is given below:-

For Property

= 25,500 × $46

= $1,173,000

For Treasure stock

= 25,500 × $40

= $1,020,000

For Additional paid-in-capital

= $1,173,000 - $1,020,000

= $153,000

Answer:

portfolio's standard deviation = 6.18%

Explanation:

we must first determine the expected returns for each stock:

stock A = (0.15 x 31%) + (0.6 x 16%) + (0.2 x -3%) + (0.05 x -11%) = 13.1%

stock B = (0.15 x 41%) + (0.6 x 12%) + (0.2 x -6%) + (0.05 x -16%) = 11.35%

stock C = (0.15 x 21%) + (0.6 x 10%) + (0.2 x -4%) + (0.05 x -8%) = 7.95%

then we must determine the variance of each stock's return:

stock A = {[0.15 x (31 - 13.1)²] + [0.6 x (16 - 13.1)²] + [0.2 x (-3- 13.1)²] + [0.05 x (-11 - 13.1)²]} / 4 = (48.0615 + 5.046 + 51.842 + 29.0405) / 4 = 33.4975

stock B = {[0.15 x (41 - 11.35)²] + [0.6 x (12 - 11.35)²] + [0.2 x (-6- 11.35)²] + [0.05 x (-16 - 11.35)²]} / 4 = (131.868375 + 0.2535 + 60.2045 + 37.401125) / 4 = 57.4219

stock C = {[0.15 x (21 - 7.95)²] + [0.6 x (10 - 7.95)²] + [0.2 x (-4- 7.95)²] + [0.05 x (-8 - 7.95)²]} / 4 = (25.545375 + 2.5215 + 28.5605 + 12.720125) / 4 = 17.3369

portfolio's variance = (0.3 x 33.4975) + (0.4 x 57.4219) + (0.3 x 17.3369) = 38.21908

portfolio's standard deviation = √38.21908 = 6.18%

Answer:

Enterprise value = $ 3,033

Explanation:

The enterprise value is full value of business. It includes total equity and debt. However cash and cash equivalent are not included in it. Detail calculations are given below.

Enterprise Value = Market value of equity/common stock + Total debt- Cash

MV of equity = 24.5 * 118 = $ 2,891

Total Debt = 688/2*3 = $ 1,032

Cash = ($ 890)

Enterprise value = $ 3,033

Answer:

C) 8.15 percent

Explanation:

The computation of the abnormal return for the two week period is as follows:

Abnormal return is

= (1 + first week abnormal return) × (1 + second week abnormal return) - 1

= (1 + 5%) × (1 + 3%) - 1

= 1.0815% - 1

= 8.15%

Hence, the correct option is c.

We simply applied the above formula so that the correct value could come

And, the same is to be considered

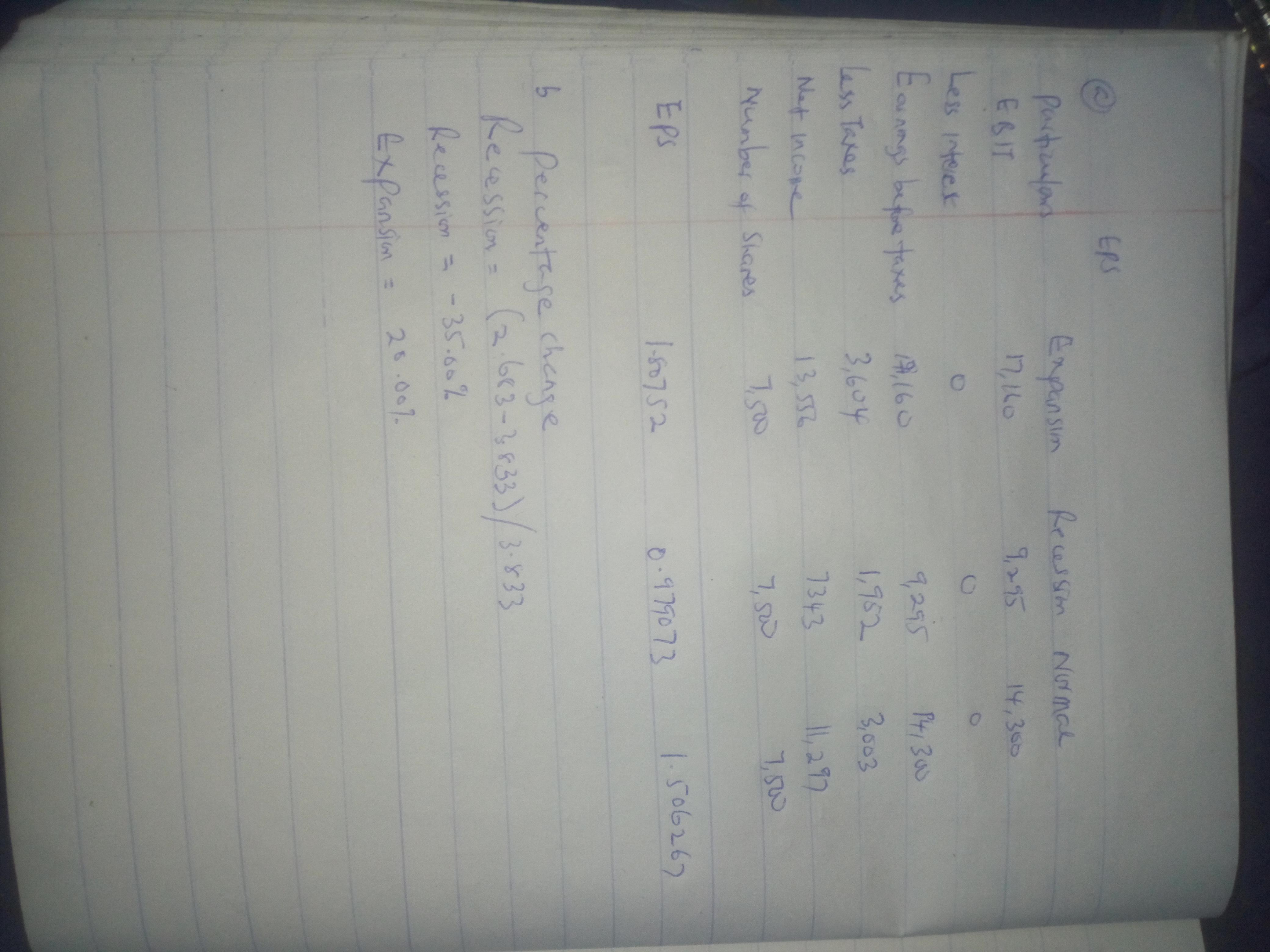

Answer:

Please see attached.

Explanation:

a. Calculate earnings per share EPS under each of the three economic scenarios

a.2 Calculate the percentage changes in earnings per share EPS for economic expansion, or recession.

b-i calculate economic per share EPS, under each of the three economic scenarios after recapitalisation.

b-2 calculate the percentage changes in EPS when the economy enters or expand a recession assuming no recapitalisation occurred.

Please find attached detailed solution to the above questions.