Answer:

Explanation:

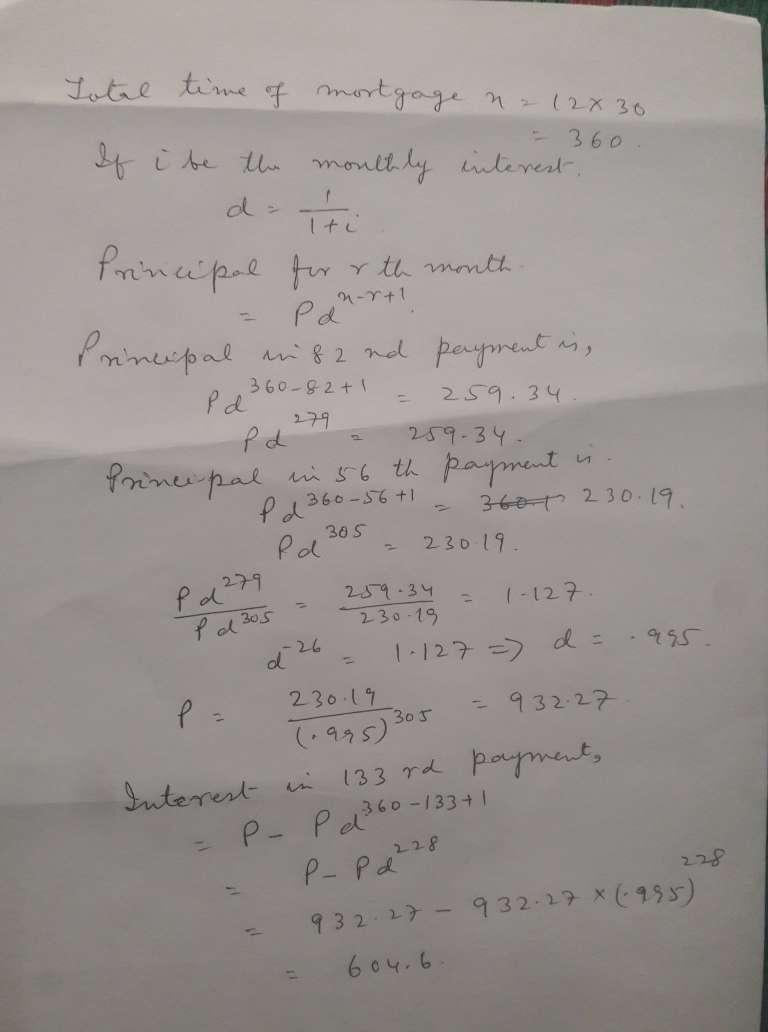

See attached file for answer

Answer:

Annual demand (U) = 90.000 bags

Cost of each bag = $1.50

Inventory carrying cost per unit(C) = $1.50 × 20% = 0 30

Ordering cost per unit (O) = $15

Part A)

EOQ = 3,000

Part B)

Maximum inventory = EOQ + Safety inventory on hand

Maximum inventory = 3000 + 1000

Maximum inventory = 4.000

Part C)

Average inventory = Maximum inventory + Minimum or Safety /2

Average inventory = 4,000 + 1,000 / 2

Average inventory =2,500

Part D)

How often company order = Annual demand / EOQ

How often company order = 90,000 / 3.000

How often company order = 30

Answer:

oligopoly

Explanation:

An oligopoly is a market structure comprising a few firms dominating a large market with many buyers. The few firms sell similar or differentiated products. Each of the firms commands a sizable market share and can influence the market. Apart from the few dominating firms, there could be other small sellers with a smaller market share operating in the market. Another example of an oligopoly market is the air travel business, where a few airline companies dominate the market.

Characteristics of oligopoly market include

- Barriers to entry due to heavy capital requirements and market domination by a few firms.

- Each firm sets its price

- heavy advertising to woe clients

- Collaboration among the few dominating firms

Answer:

The correct answer is:

Equilibrium price will decrease; the effect on quantity is ambiguous. (D)

Explanation:

First, note that if the price of coffee beans, used in the manufacture of coffee decreases, the price of coffee sold to consumers will decrease, because it takes a lesser amount in manufacturing than it used to, therefore this reduction in manufacturing costs is reflected in the selling price.

Next, it is hard to tell whether this reduction in equilibrium price will affect quantity demanded, because, at the same time, the price of cream ( a complementary good) increases, and since both goods are complementary, they are bought together, and the effect of the reduction in the price of coffee might not necessarily caused an increase in the quantity demanded because this effect is cancelled out by the increase in the price of cream, hence the effect on quantity is ambiguous.

Answer:

a) $28 Million

b) -$24 Million

Explanation:

The first part of the question is to determine the pension liability tht should be reported in the balance sheet

To do this, we use the following formula

Projected Benefit Obligation - The Plan Assets

= $65 million - $37 Million = $28 Million

Part B) This part says to dettermine the amount JDS would report if the planned asset increase to $89 million

The formula Projected Benefit Obligation - The Plan Assets still should be used but there is a difference as follows

$65 million - $89 Million = -$24 Million