Answer:

$4,424

Explanation:

Calculation to determine what amount would you have lowered your federal income tax

Using this formula

Reduction in Federal income tax amount = (Mortgage interest + Real estate taxes) x Tax rate

Let plug in the formula

Reduction in Federal income tax amount= ($13,200 + 2,600) x 0.28

Reduction in Federal income tax amount=$15,800×0.28

Reduction in Federal income tax amount = $4,424

Therefore The amount that you would have lowered your federal income tax is $4,424

Answer:

I think it would be the first one to be honest

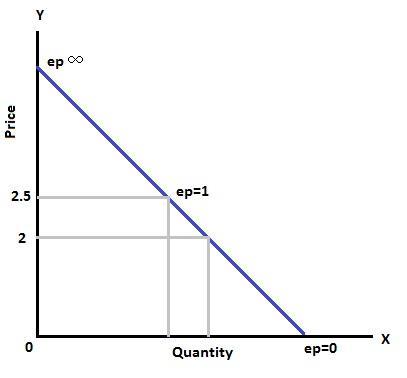

Answer:

The correct answer is option A.

Explanation:

The demand for cantaloupes is unitary elastic at price level $2.50. The demand curve here is linear and downward sloping. The elasticity of demand is 1.

In this linear demand curve the lower portion will represent inelastic demand.

When the price level is reduced to $2 the demand will move to the lower portion of the curve, with fall in price and increase in demand.

So, at $2 price the demand will be inelastic, which means it will be between 0 and 1.

Answer:

The correct answer is: enter the market; exit the market.

Explanation:

In a perfectly competitive market, there is no restriction on entry and exit of firms. So profits will attract other potential firms to join the market. And when the existing firm incurs losses it will cause them to stop operating and exit the market.

Because of this, the firms in competitive settings are motivated to produce at a low cost and they come up with new ideas to please customers so that they earn a profit.

Answer:

The part of economics concerned with single

factors and the effects of individual decisions.

Explanation:

Hope this helps!