Marginal analysis is really important for a firm. Marginal analysis helps a firm to determine the most equitable allocation of a firm’s resources.

EXPLANATION:

Marginal analysis is an assessment of additional benefits of a firm activity, compared to the additional costs which are incurred by the exact same firm’s activity. A firm or company applied marginal analysis to make a decision which helps a firm to maximize the potential profits and benefits. The example of marginal analysis is when the firm’s cost to produce one more appliance or the profit gained by adding one more worker.

In microeconomics, marginal analysis is applied to analyze how a compound system being influenced by marginal manipulation of its comprising variables. On this occasion, the marginal analysis focuses on investigating the results of small changes as the consequences cascade across the business as a whole. The goal of marginal analysis is to investigate whether the costs associated with the change in activity will affect in a benefit which is sufficient enough to offset a firm. The whole impact of marginal analysis is on the cost of producing an individual unit which is most often observed as a comparison’s point.

LEARN MORE:

If you’re interested in learning more about this topic, we recommend you to also take a look at the following questions:

1. Marginal analysis helps to? brainly.com/question/3318349

2. A command economy tends to exist under a brainly.com/question/10877298

KEYWORDS: marginal analysis, economy analysis

Subject: Business

Class: 10-12

Sub-chapter: Marginal Analysis

Answer:

2.02

Explanation:

Each pail of plaster covers 97 Square feet of ceiling

The ceiling of the room is 14 ft long

= 14×14

= 196

Therefore the pail of plaster that will be needed to cover the rooms can be calculated as follows

= 196/97

= 2.02

Answer:

The correct phrase for the blank space is: creative problem solver.

Explanation:

Companies have to adapt to their customers to attract more of them, moreover, when the institutions have a presence in different regions worldwide. In such scenarios, they have to act as creative problem-solvers to adjust what the consumer desire and what the institution has projected to offer.

Firms must conduct different market research to gather more information on their target market and should study the resources it counts on to satisfy those individuals' expectations.

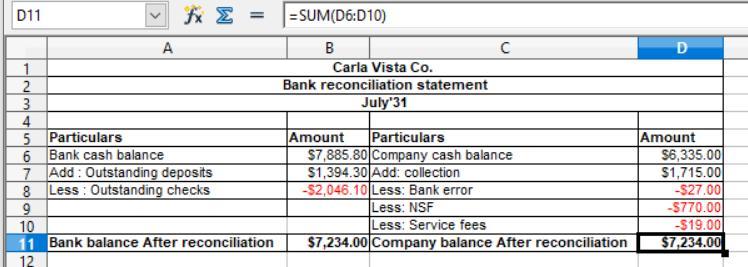

Explanation:

The preparation of the bank reconciliation statement is presented below in the attachment.

As we know that

The Bank reconciliation works with the balance of the bank statement and the balance of the cash statement. The aim is to compare those two statements to allow the organisation to operate smoothly.

There are various transactions because of which the balance of the bank statement and the balance of the cash statement do not match. We change the transactions correctly to match those statements.

The bank error is

= $374 - $347

= $27