Answer: Creativity.

Professionalism.

Risk-taking.

Passion.

Planning.

Knowledge.

Social Skills.

Open-mindedness towards learning, people, and even failure.

Answer: Passive wiretap

Explanation: passive wiretap is the monitoring or recording of data that attempts only to observe a communication flow and gain knowledge of the data it contains, but does not alter or otherwise affect that flow. Wiretapping is a process in which passive devices are used to monitor or record data that are being transmitted in a line or a loop, Passive wiretapping happens when attackers are trying to obtain users information through the communication channel.

Answer:

b. inventory for $1516.

Explanation:

Term 2/10, n/30 means there is a discount of 2% is available on payment of due amount within discount period of 10 days after sale and net credit period of 30 days.

Purchase value = $83,000

Purchases return = $7,200

Amount Due = $83,000 - $7,200 = $75,800

As the $75,800 is paid within discount period, so discount will be given to customer

Discount = $75,800 x 2% = $1,516

Payment Made = $75,800 - $1,516 = $74,284

Gross method does not record the discount value it recognise the inventory at its gross amount and discount is adjusted in the inventory account after that.

Answer:

The Board of Governors--located in Washington, D.C.--is the governing body of the Federal Reserve System. It is run by seven members, or "governors," who are nominated by the President of the United States and confirmed in their positions by the U.S. Senate.

Explanation:

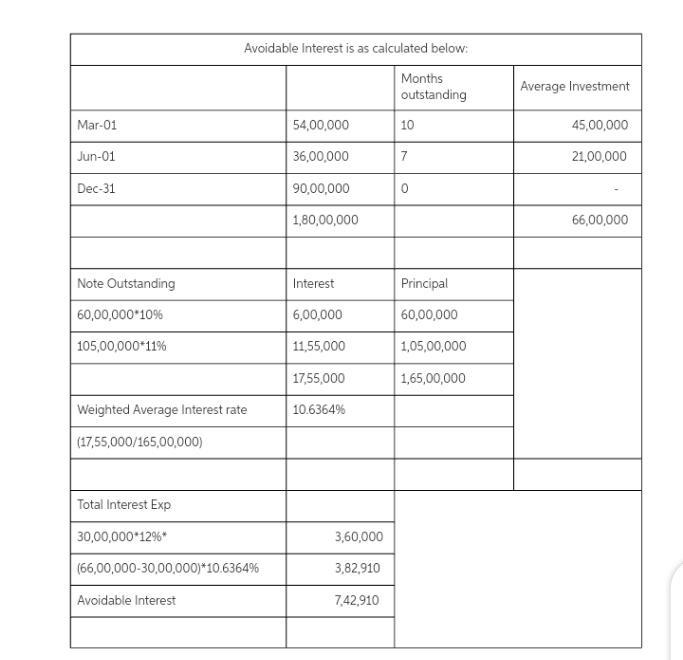

Answer: $742910

Explanation:

The weighted average combines interest rates into a single interest rate which yields a combined cost which is about thesame as cost of the original separate loans.

The weighted-average interest rate for interest capitalization purposes for the company above is calculated in the attachment below.