To obtain (goods or a service) from an outside or foreign supplier.

You will have a negative amount of moneyz in your checking account.(You will owe moneyz)

Unlimited liability and separate taxation of the business are advantages of a sole proprietorship.

The statement is False.

<h3>What is taxation ?</h3>

In practically every nation on the planet, governments impose taxes as mandatory levies on people or organizations. Although it can be used for other things as well, taxes are typically utilized to finance government spending.

Taxes are imposed on tangible property, including real estate and business dealings like stock sales or home purchases. Taxes exist in a variety of forms, including income, corporation, capital gains, property, inheritance, and sales taxes.

A fundamental method for nations to produce public revenues that enable them to support investments in human capital, infrastructure, and the provision of services for residents and enterprises is through the collection of taxes and levies.

To learn more about taxation from the given link:

brainly.com/question/1980107

#SPJ4

Answer:

balanced scorecard

Explanation:

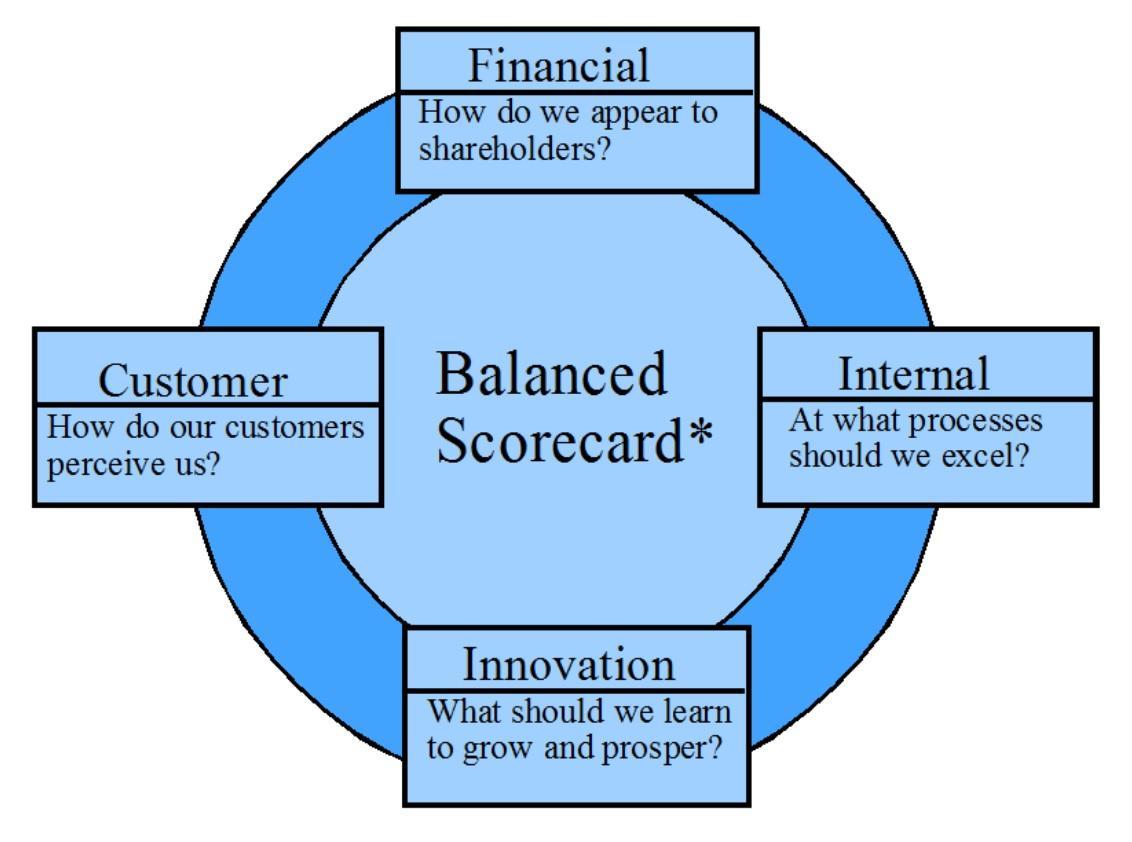

The term that is being mentioned in this question is known as a balanced scorecard. This is a strategic management performance metric that is used to measure and provide feedback to a company's management by identifying and improving different internal business functions and their outcomes, usually in regards to the employees themselves. An example of a balanced scorecard can be seen in the attached photo.

Answer:

The correct answer is workforce Polarization.

Explanation:

Polarization means that a gap has developed in the job market, with most employment opportunities at the lowest and highest levels and few jobs for those with midlevel skills and education. At one end, there has been strong demand for low-skilled, low-paying jobs in industries like food service and retail. On the other end, some research shows that in certain fields there has been a steadily increasing demand for highly skilled and educated professionals, technologists, and managers. These high-skilled positions also tend to be highly paid.