Answer:

-22.

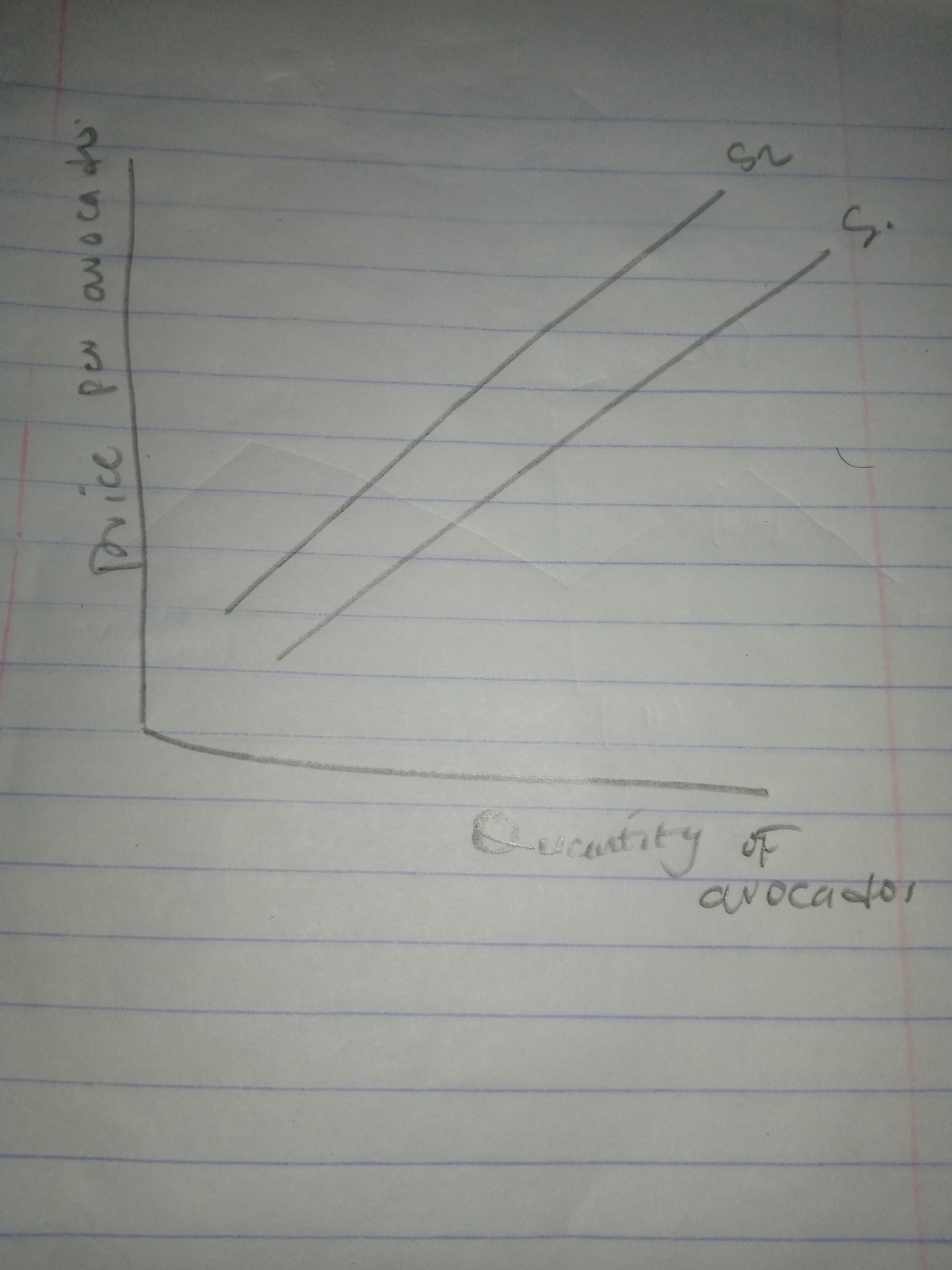

There will be the decrease in price hence the supply curve shifts to the left.

Explanation:

So, it is given from the question above that the supply function for avocados is Q = 58 + 15p - 20p_f.

The p_f given in the question = $1.10 which is the price given for the fertilizer as it rises that is to say it rises at that amount.

If the price increases by $1.10, then we have a reduction of -( 20 × 1.10) = -22.

Kindly note that the negative sign denotes the reduction in supply. This reduction causes the supply curve to shift to the left.

The diagram for the supply curve Is given in the attached picture.

The three key approaches that are needed in entering international

markets include the following; direct investment, exporting and even joint

venturing. These are three key approaches that will complete the space provided

above as this is where the company decide on how a chosen market long dash may

enter.

When accounting for a long-term construction contract under IFRS, if the percentage-of-completion method is not appropriate, the seller should account for revenue using "cost recovery method".

<h3>What is cost recovery method?</h3>

According to the "Cost Recovery Rule," any excess cash value (cost basis) over premium payments that results from a partial withdrawal of cash or a policy surrender is taxable income.

Calculation for cost recovery method includes:

- the product's operating expenses, such as those for hardware, software, and labour, should all be added up.

- Analyse whole revenue, regardless of whether a client made a lump-sum payment or several instalments.

- To calculate the profit, deduct the cost of products from whole sales.

To know more about the lump-sum payment, here

brainly.com/question/23220127

#SPJ4

Answer:

Credit life Insurance

Explanation:

The scenario describes Credit life insurance

This is a form of insurance policy that that is designed to pay off the balance on a policy holder's outstanding loan in case of death. It is designed for the protection of lender and heirs who are co signers from loss in case of the death of the borrower.

The insurance is liable to the balance on the loan as at the time of the death of the borrower.