Answer:

Answer is explained in the explanation section.

Explanation:

Note: First of all, this question is incomplete and lacks necessary data to calculate this question. However, I have found the similar question on the internet with complete data given. Additionally, I have shared that data as well in the attachment below for your convenience, Thanks.

Solution:

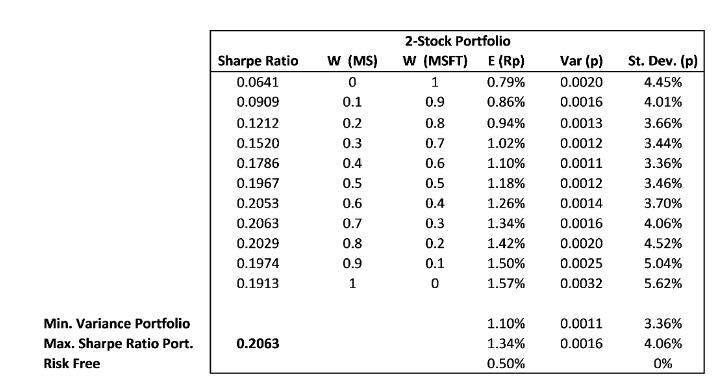

SD = Standard Deviation

Using utility function, E(R) = Rp - 0.005 x A x  = 1.34 - 0.005 x 3x

= 1.34 - 0.005 x 3x

Using utility function, E(R) = 1.093%

If the weight in the risky portfolio is let's say, "a" then,

weight in the risk-free asset = 1 - a

So,

E(R) = a x Rp + (1 - a) x Rf

1.093% = a x 1.34% + (1 - a) x 0.50%

Solving for "a"

a = 70.56% - weight in risky portfolio

and 1 - a = 29.44% - weight in risk-free asset.

Similarly, if you want a return of 1.10%,

we can follow the above steps and get

1.1% = a x 1.34% + (1 - a) x 0.5%

Weight in risky portfolio,

a = 71.43%

weight in risk-free asset,

1 - a = 28.57%