Answer:

8,000

Explanation:

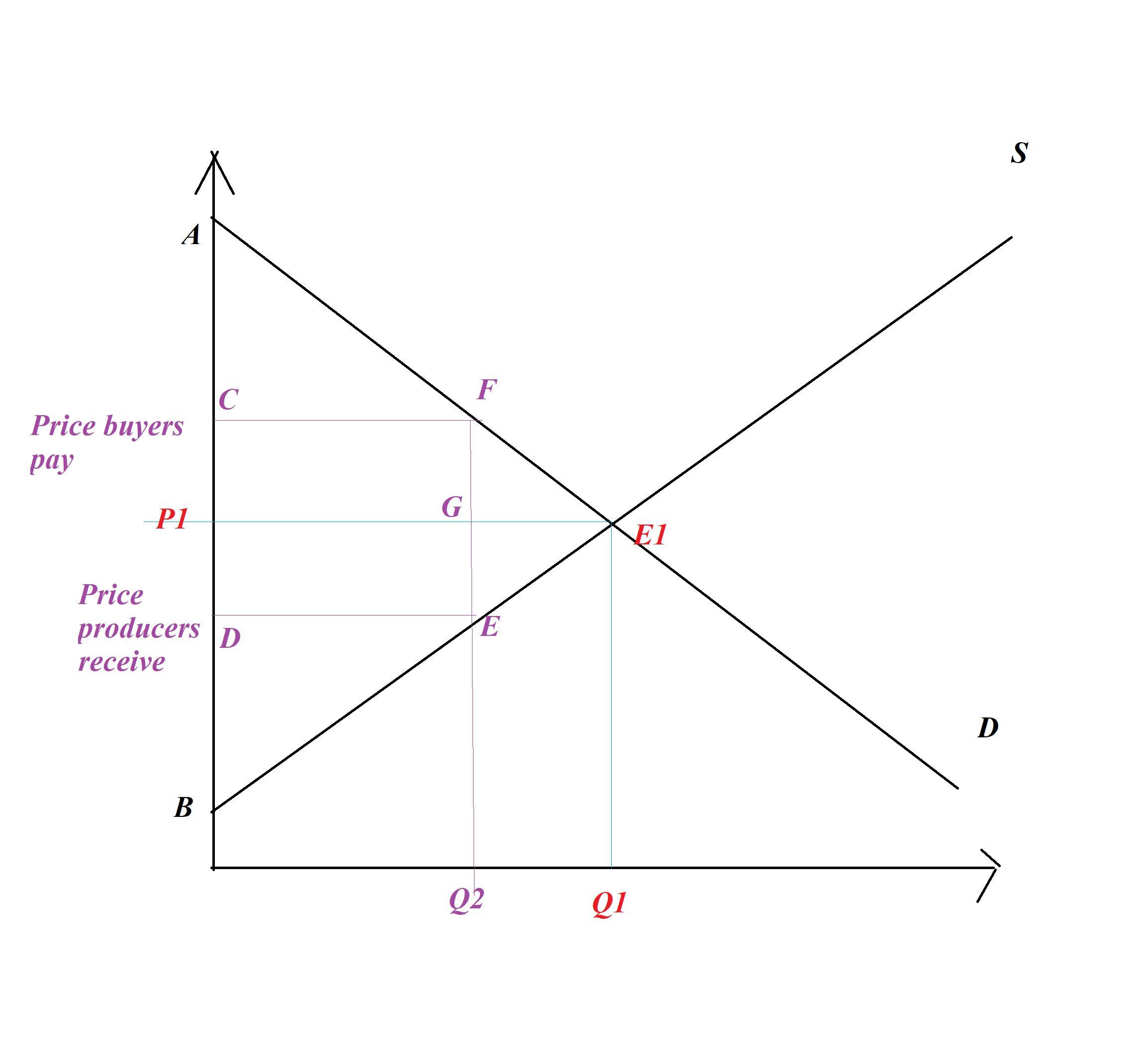

Initially, the market is at equilibrium E1: P = P1; Q = Q1

Assume that the tax is imposed, the market will move to when Q = Q2; the price buyers pay is greater than P1, the price producers receive is less than P1.

We have: <em>Price buyers pay - Price producers receive = Tax</em>

As the tax decreases the equilibrium quantity by 700 headphoes

=> Q1 - Q2 = 700

=> Q2 = Q1 - 700

=> Q1 + Q2 = Q1 + Q1 - 700 = 2Q1 - 700

Before tax:

+) the producer surplus (PS) is equal to the area formed by supply curve S, price line P1 and the vertical axis

=> PS1 = Area of BE1P1

+) the consumer surplus (CS) is equal to the area formed by demand D, price line P1 and the vertical axis

=> CS1 = Area of AE1P1

=> The wellness before tax = CS1 + PS1 = Area of AE1B

After tax:

+) the producer surplus (PS) is equal to the area formed by supply curve S, price line (Price producers receives) and the vertical axis

=> PS2 = Area of BDE

+) the consumer surplus (CS) is equal to the area formed by demand D, price line (price buyers pay) and the vertical axis

=> CS2 = Area of ACF

+) The Tax revenue = Tax * Q2 = (Price buyers pay - Price producers receive) * Q2 = CD * DE = Area of CFDE

=> The wellness after tax = PS2 + CS2 + Tax Revenue = BDE + ACF + CDEF

=> Deadweight loss = Wellness before Tax - Wellness after tax = Area of EFE1 = 2,800

The tax decreases consumer surplus by $4,000.00, and it decreases producer surplus by $6,800.00

So that:

+) CS1 - CS2 = 4,000

=> Area of AE1P1 - Area of ACF = Area of CFE1P1 = 4,000

+) PS1 - PS2 = 6,800

=> Area of BE1P1 - Area of BDE = 6,800

=> Area of EDP1E1 = 6,800

=> Area of CFE1P1 + Area of EDP1E1 = 4,000 + 6,800

=> Area of CFE1ED = 10,800

Area of CDEF + Area of EFE1 = Area of CFE1ED = 10,800

=> Area of CDEF + 2,800 = 10,800

=> Area of CDEF = 8,000

=> Tax revenue = 8,000