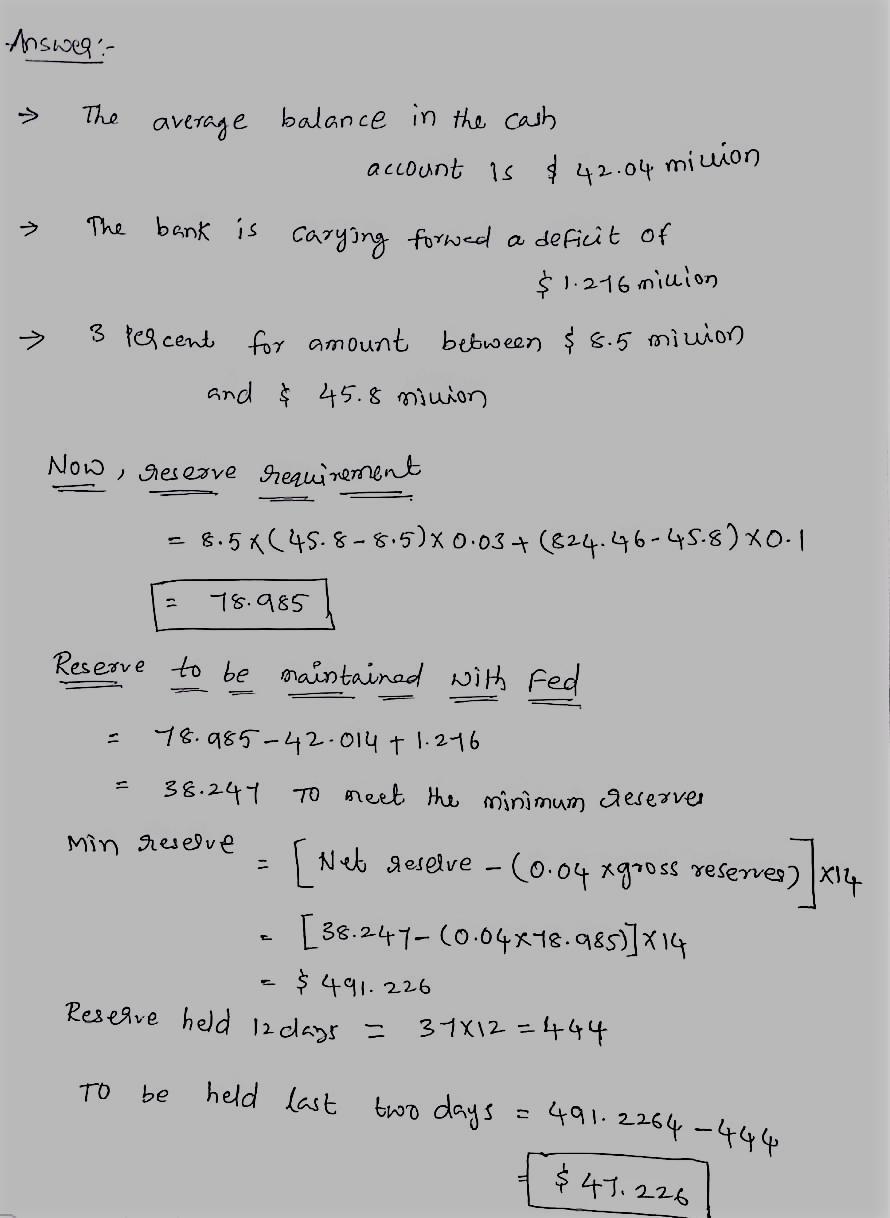

Answer:

$ 20= Q1 (0.5 ) + Q3( 3)

Explanation:

Total Amount = $ 20

Dental treats Q2= $ 3

Catnip Q1= $ 0.50

Maximum no of Dental Treats he can get is = $ 20 /$3= 6.66

If he gets maximum dental treats i.e 6 , $18 will be spent (3*6)

He will be left with = $ 20- $ 18= $ 2

The maximum no of catnip he can get after buying 6 dental treats from $ 2= $ 2/$0.5= 4

Let Q1 denote the catnip and Q3 denote the dental treats then the equation would be like

$ 20= Q1 (0.5 ) + Q3( 3)

So putting the values for q1=0,1,2,3,4,5,6,7,8,9,10

for values 0-4 Q3 will be $ 18

for values 4-6 Q3 will be $ 15

for values 6-8 Q3 will be $ 12

From values Zero on wards the budget constraint will be a slope but after value 4 the change will be after every two points.

The slope will look like the one given in the diagram.