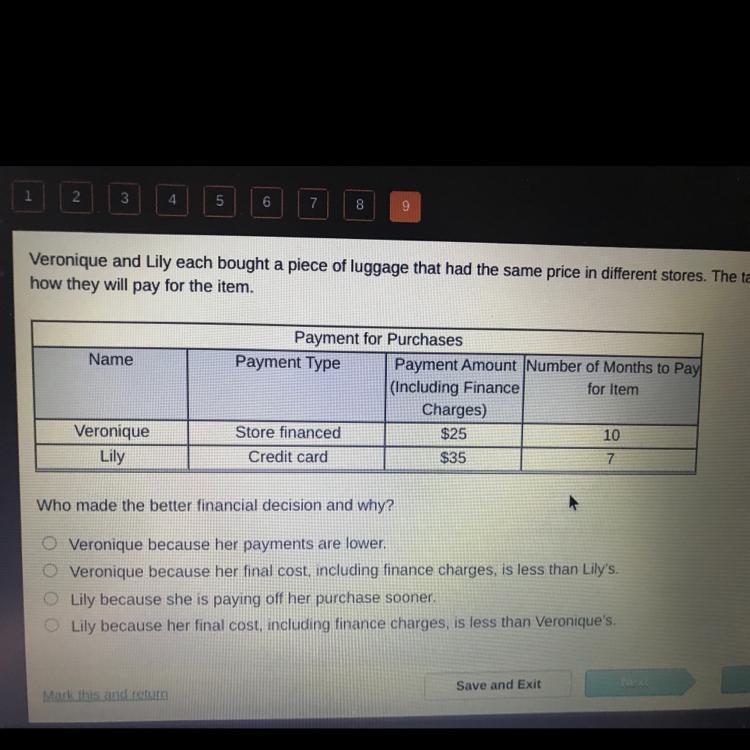

According to the information in the Graph Veronique made a better decision than Lily because the final cost of her purchase is lower including finance charges (option B)

<h3>What is a finance charge?</h3>

A finance charge is an economic term that refers to additional charges made by finance companies (such as banks) to a transaction we make, such as a purchase.

In the case of Veronique and Lilly, they both bought the same suitcase with different prices. However, the better financial decision was Veronique's because she paid less ($25) for the same bag including finance charges.

While Lilly, despite having fewer fees, will have to pay $10 more than Veronique.

Note: This question is incomplete because the image is missing. Here is the image.

Learn more about payment in: brainly.com/question/15138283

Answer:

a price floor set above equilibrium

Explanation:

A price floor is a concept to prevent prices from being too low. Generally, it is used by governments to prevent the rights of supplier and sellers. A horizontal line above the equilibrium depicts price floor. Usually, if a price is set above the equilibrium, excess supply or surplus of commodities take place which results in a decrease in the prices. This is why the price floor is normally set at equilibrium.

Answer:

C) 3

Explanation:

The current ratio is the firms Current assets relative to its current liabilities.

It can be calculates as follows,

Current Ratio = Current assets / Current liabilities

Current Ratio = 240,000 / 80,000

Current ratio = 3

This signifies a healthy ratio as the company has 3 times as much current assets as compared to its current liabilities.

Hope that helps.

1 - performed an illegal act (actus reus)

2-while performing the act , had the required intent or specific state of mind ( mens rea)