Answer:

b. As income increases, the quantity demanded of food decrease

Explanation:

food weights for individuals whose income is sufficient enought to keep them healty and feed will not increase their food consumption much else. That's because, their already have it covered and want to saisfy new needs

The demand for food is only high at low levels of income.

Assuming Raleigh BBQ has $48,000 in current assets and $39,000 in current liabilities. This refers to as working capital management.

<h3>What is Working Capital Management?</h3>

Working capital management can be defined as the way in which a company or an organization ensures that both their current asset and current liabilities are put in use effectively and efficiently.

A company who make use of working capital management as a strategy will tend to ensure that their liabilities does not exceed their assets so as to maintain the company financial health.

Therefore this refers to as working capital management.

Learn more about working capital management here:brainly.com/question/14736085

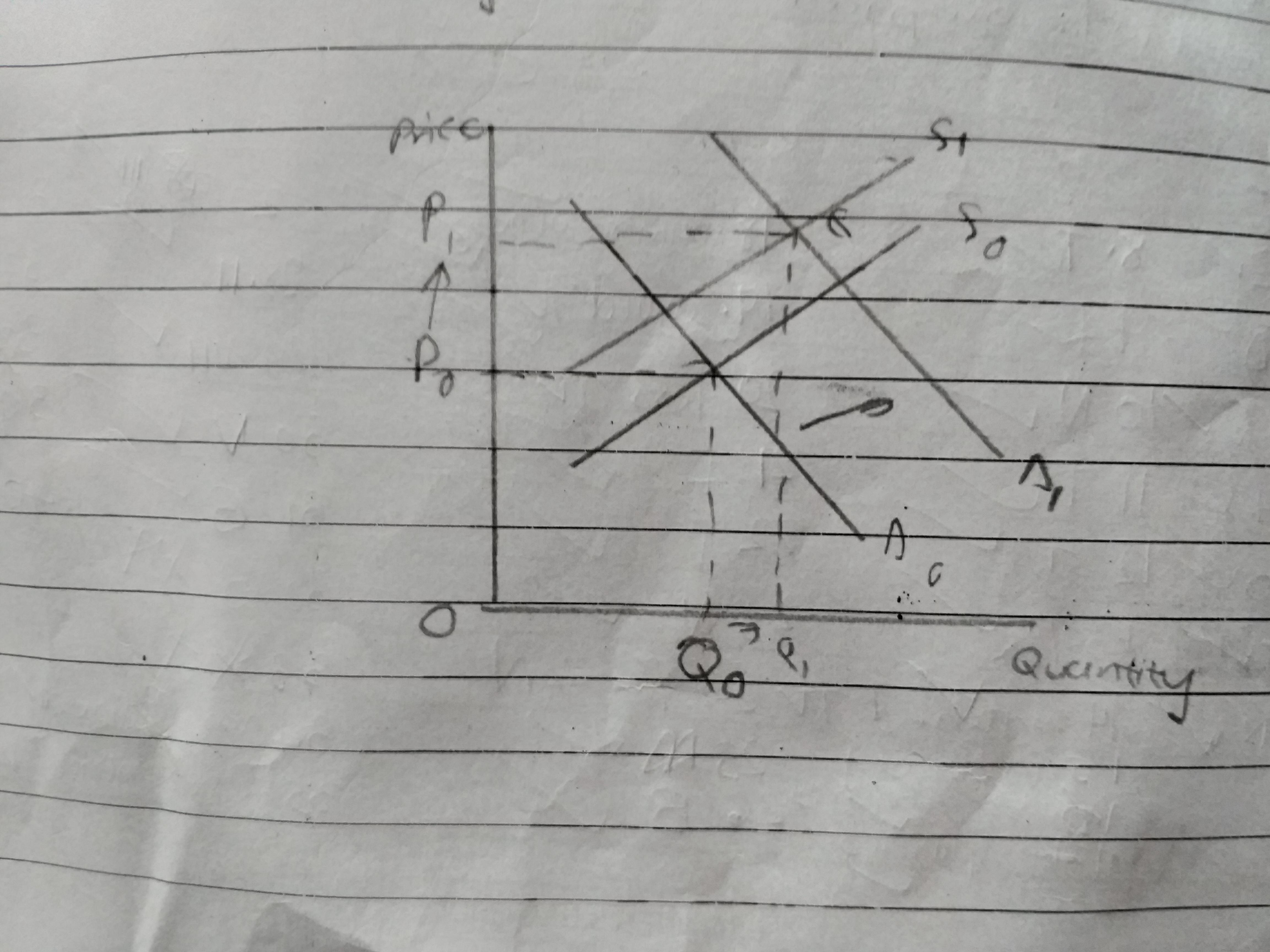

Answer:

Rises

Rises

Explanation:

If the demand for a good rises more than the fall in supply, both equilibrium price and quantity would increase.

Refer to the attached image for a graphical explanation.

I hope my answer helps you

Read from this following website this will answer your question it answered mine.

If this is helpful plz tell me it will tell you all about your question.

<span>http://smallbusiness.chron.com/happens-contribution-margin-company-negative-22905.html

</span>