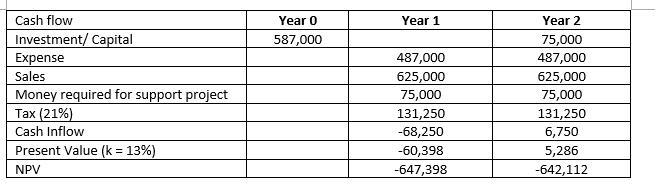

Answer:

The cash inflows in Year 2 is: $6,750

The present value of the project in Year 2 is: $5,286 (ignored the depreciation)

The Net Present Value in Year 2 is: $-642,112 (required return rate is 13%)

Explanation: <em><u>(See the attached table also)</u></em>

1. Initial investment: $587,000

2. Year 1:

- Sales: $625,000

- Cash expense: $487,000

- Money to support project: $625,000 x 12% = $75,000

- Tax to pay: $625,000 x 21% = $131,250

=> Cash inflow in Year 1:

625,000 - 487,000- 75,000 - 131,250 = - 68,250

Present value: -68,250 : (1+0.13) = -60,398

NPV: -60,398 - 587,000 = - 647,398

Year 2:

- Capital from year 1: $75,000

- Sales: $625,000

- Cash expense: $487,000

- Money to support project: $625,000 x 12% = $75,000

- Tax to pay: $625,000 x 21% = $131,250

=> Cash inflow in Year 2:

75,000 + 625,000 - 487,000- 75,000 - 131,250 = 6,750

Present value: 6,750 : [(1+0.13)^2] = 5,286

NPV year 2 = NPV Year 1 + PV Year 2 = -647,398 + 5,286 = -641, 112