Answer:

Option (d) $86,864

Explanation:

Present value = Cash flow × Discounting factor

Here,

Discounting factor = ( 1 + r )⁻ⁿ

n = the year of cash flow

r = discount rate = 12%

Year (n) Cash flow Discount factor Present Value

3 $11,000 0.71178 $7,830

5 $50,000 0.567427 $28,371

6 $1,00,000 0.506631 $50,663

Therefore,

The amount he or she should pay for the investment today

= ∑(Present value)

= $7,830 + $28,371 + $50,663

= $86,864

Hence,

Option (d) $86,864

Answer:

$1,333

Explanation:

The computation of the deprecation expense is shown below:

= (Original cost - residual value) ÷ estimated useful life

= ($23,000 - $3,000) ÷ 5 years

= $4,000

This $4,000 depreciation expense come for a year but the asset is purchased on September 1, 2019 and the books are closed on December 31, 2019

So, the four months depreciation expense would be

= Yearly depreciation expense × number of months ÷ (total number of months in a year)

= $4,000 × (4 months ÷ 12 months)

= $1,333.33

The four months is calculated from September 1 to December 31

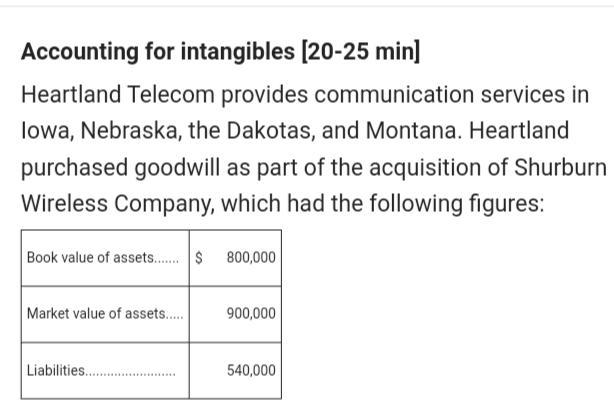

Answer: 1. Goodwill

2. a. Record no entry in the books

b. Record a loss in the books

Explanation:

1. The Special asset created by Heartland Telecom's acquisition of Surety Wireless is Goodwill.

Goodwill is the difference between what the company was worth and what it was purchased for if the purchase price was higher than the worth (market value).

2. a. Goodwill should be accounted for by recoding it in the Long term Assets under Intangible Assets in the balance sheet. It should not be amotrized. If Goodwill increases, there should be no recording this <u>gain</u> on the books.

b. If the value of the asset has decreased, Heartland should record a loss in the books to represent the loss on this account.

Answer:

The 3 represents the percentage of cash discount. It means the cardholder will receive a 3% discount if the bill is paid within 15 days from the billing date.