Answer:

1. FIFO inventory is greater than (>) LIFO inventory.

2. FIFO cost of goods sold is less than (<) LIFO cost of goods sold.

3. FIFO net income is greater than (>) LIFO net income.

4. FIFO income taxes are greater than (>) LIFO income taxes.

b. Income shown on the company’s tax return would be lower if LIFO rather than FIFO is used.

Explanation:

FIFO and LIFO are accounting methods used in managing costs related to inventory, stock repurchases at different times and financial activities associated with monetary costs a company had tied up within inventory of feedstocks, raw materials, produced goods, and equipment parts.

Simply stated, FIFO and LIFO are accounting methods is used for the valuation of the cost of goods sold and ending inventory of a company.

FIFO is an acronym for "First In, First Out" and it assumes oldest unit of inventory is sold first, meaning goods that were first added to inventory are the first goods removed from inventory for sale and are recorded as sold first.

LIFO is an acronym for "Last In, First Out" and it assumes last unit to arrive in inventory is sold first, meaning goods that were last added to inventory are the first goods removed from inventory for sale and are recorded as sold first.

Answer:

many other sellers are offering a product that is essentially identical.

Explanation:

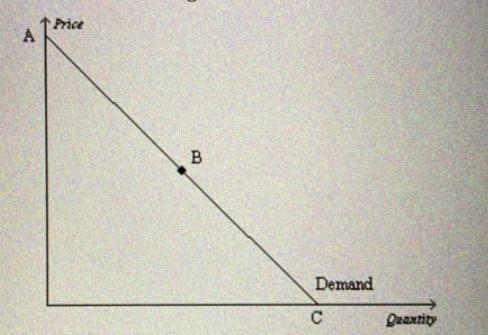

Answer: d. elastic section of the demand curve.

Explanation:

When using a linear demand curve, it has been found that the top half of the curve represents the elastic section which is where the section A to B cover so this is the elastic section.

The mid point which is B here is the unitary elastic portion of the curve and the bottom half of point B to C is the inelastic section.

In the elastic section, increasing the price by a certain percentage would cause the quantity demanded to fall by a higher percentage than the percentage increase in price.

Answer: Recommend that such borrower should contact the representative of the lender before the signing of the documents.

Explanation:

In a scenario whereby a borrower is questioning the amount of the notary or the signing fee that appears on the settlement statement, the notary agent should simply tell the borrower that he or she should contact the representative of the lender before the signing of the documents.

If that is done, the borrower can then know the next thing to do after hearing from the lenders representative.

Answer:

(a) $23,800

(b) $20,400

Explanation:

(a) Donna purchased the stock on December 28, 2018 and sold it on September 10, 2019. This means she held the stock for less than 1 year. Hence, she made a short-term capital gain that is treated as ordinary income property for tax purposes.

As per rules, the tax deduction for ordinary income property is the lesser of the adjusted basis and fair market value, that is, the lesser of $23,800 and $34,000. Therefore, the deduction is $23,800.

(b) Again, we compare the adjusted basis and fair market value. In this case, the fair market value is $20,400 which is less than the adjusted basis of $23,800. Therefore, the deduction is now $20,400 only.