Answer:

1) Cost of equity is 12.501%

2) Price of bond is $935.82

3) Price of semi-annual bond is $934.96

Explanation:

1) Given:

Beta = 1.1

Risk free rate (Rf) = 3.25%

Market risk premium (Rp) = 8.41%

Using CAPM to compute cost of equity:

Re = Rf + β (Rp)

= 3.25 + 1.1(8.41)

= 12.501%

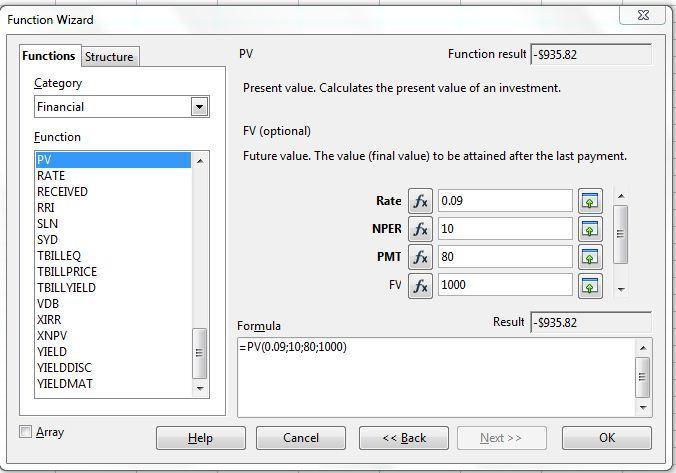

2) Price of bond is present value of bond.

Face value (FV) = $1,000

Maturity (nper) = 10 years

Coupon rate = 8%

Coupon payment (PMT) = 0.08× 1000 = $80

Discount rate (rate) = 9% or 0.09

Using spreadsheet function =PV(rate,nper,pmt,FV)

Price of bond is $935.82. It is negative as it's cash outflow

3) Price of semi-annual bond is present value of bond.

Face value (FV) = $1,000

Maturity (nper) = 10×2 = 20 periods

Coupon rate = 8% ÷ 2 = 4%

Coupon payment (PMT) = 0.04× 1000 = $40

Discount rate (rate) = 9% ÷ 2 = 4.5% or 0.045

Using spreadsheet function =PV(rate,nper,pmt,FV)

Price of semi-annual bond is $934.96