Answer:

The price of building materials suddenly going up.- B.

Answer:

C. an increase in accrued expenses

Explanation:

Operating activities: It includes those transactions which affect the working capital after net income. The increase in current assets and a decrease in current liabilities would be deducted whereas the decrease in current assets and an increase in current liabilities would be added.

These changes in working capital would be adjusted. Moreover, the depreciation expense is added to the net income and the loss on the sale of assets is added whereas the gain on sale of assets is deducted

I would say 4

Hope this helps!!

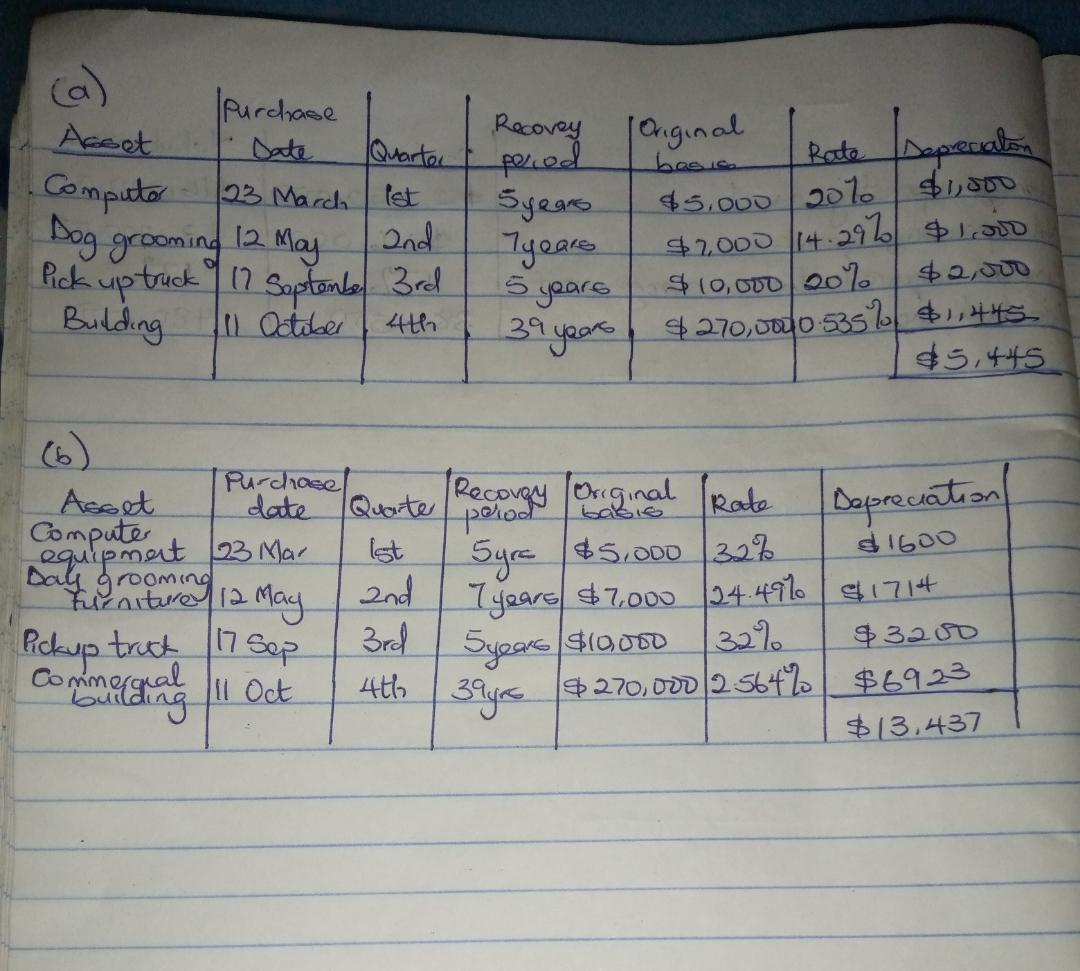

Answer: See attachment

Explanation:

a. What is Poplock’s year 1 depreciation expense for each asset?

See attachment. Note that the depreciation for the assets were calculated as the original basis × the rate. e.g for Computer equipment, the Depreciation was, the original basis of $5000 × the rate of 20% which equals $1,000.

b. What is Poplock’s year 2 depreciation expense for each asset?

Check attachment.

Depreciation for computer = $1600

Depreciation for day grooming furniture = $1714

Depreciation for popup truck = $3200

Depreciation for commercial building = $6923

Answer:

i want to see the answer to this question