Answer:

the full cost of the product per unit if the marketing costs is $3,000 is $7,025.

Explanation:

The cost of the special order will exclude the Fixed manufacturing support as these are common whether the order is accepted or not thus irrelevant. Remember to include the marketing costs as an additional cost.

Calculation of cost of the product :

Direct materials $1,825

Direct labor $900

Variable manufacturing support $1,300

marketing costs is $3,000

Total $7,025

Conclusion :

Thus, the full cost of the product per unit if the marketing costs is $3,000 is $7,025.

Answer:

HR is responsible for key systems and processes which can underpin effective delivery of messages the organisation wishes to convey about ethics. HR and the Ethics function can work together to develop an employee incentives system for their organisation to reward employees who demonstrate ethical behaviours

Explanation:

Answer:

Explanation:

When a payment is made to somebody, you debit the receiver of that payment and credit Cash or Bank as money is paid from cash or by means of cheque. When money or cheques are received, you credit the person who is paying you and you debit the cash or bank.

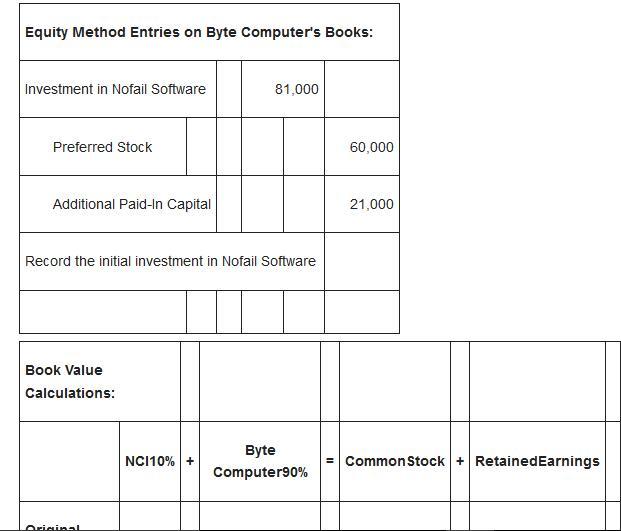

Answer: Step by step explanation of the consolidated balance sheet is given in the attached document.

Explanation:

Consolidated Balance Sheet

A consolidated balance sheet presents the assets and liabilities of a parent company and all its subsidiaries on a single document, with no distinctions on which items belong to which companies. If your company has $1 million in assets and it purchases subsidiaries with assets of $400,000 and $300,000, respectively, then your consolidated balance sheet will show $1.7 million in assets, and the sheet will commingle those assets. For example, in the asset section, accounts receivable will list the total amount of receivables held by all three companies.

When to Consolidate

A company must issue consolidated financial statements whenever it owns a controlling stake in another business – that is, whenever it owns more than 50 percent of that business. If the parent company owns 100 percent of the subsidiary, this is pretty straightforward. Complications arise, however, if the parent company owns a controlling stake with less than 100 percent ownership. Part of the subsidiary belongs to someone else, and that must be reflected on the balance sheet.