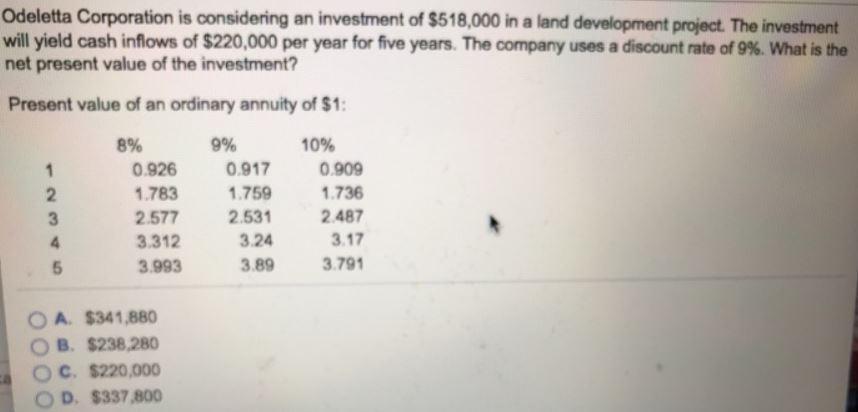

Answer: $337,800

Explanation:

Cashflow is constant so is an annuity.

The Present value of the Investment;

= Present Value of Cashflow - Investment cost

= (220,000 * Present value interest factor of an annuity, 5 years, 9% ) - 518,000

= (220,000 * 3.89) - 518,000

= 855,800 - 518,000

= $337,800

Answer:

$1,160,000.00

Explanation:

The amount of cash received during the year is the total sales revenue minus the increase in accounts receivable which is the credit sales upon which payment was not received as well as the decrease in unearned sales revenue which is the sales revenue recorded in the year but its cash was received in the prior year.

Amount of cash received during the year=$1,200,000-$25,000-$15,000=

$ 1,160,000.00

The decrease in unearned sales revenue would a debit to unearned sales revenue and a credit to sales revenue, hence it has increased sales revenue

A firm that wanted to enable its employees to use and share data without allowing outsiders to gain access could do so by establishing a: intranet

This is further explained below.

<h3>What is an intranet?</h3>

Generally, A company that intended to provide its workers the ability to utilize and exchange data while preventing unauthorized third parties from gaining access to such data may do so by building an intranet.

In conclusion, a private network built using World Wide Web technologies; is a local or limited communications network.

Read more about the intranet

brainly.com/question/19339846

#SPJ1

Answer:

How are Startups Financing Requirements Estimated?

1. Make Use of a Startup Work Sheet to be Able to Plan the Initial Financing.

2. Focus on the Expenses versus Assets. Another way for startups to estimate their financing requirements is by means of focusing on the expenses versus assets.

3. Similar Articles.

4. Cash Balance Prior to the Starting Date.

Explanation:

Answer:

c.Unlike nonprofit organizations, for-profit organizations focus on gaining competitive advantage in the marketplace.

Explanation:

The nonprofit organization is that organizations whose aim to focus on the welfare of the society as a charity, donation, etc. It can provide services in educational, research, etc,

Whereas, Profit organization is those organization whose focuses to maximizing their profit and minimizing their cost so that it would gain a competitive advantage in the marketplace. Its focuses is to target as the general public.

Hence, option c is correct