Answer: NOne of the above. Or C Place of employement

Explanation:

Answer:

Explanation:

For recording of the journal entry, first we have to compute the tax payable amount which is shown below:

Pretax accounting income tax expense = pretax accounting income × tax rate

= $210,000 × 40%

= $84,000

Tax payable for taxable income = Taxable income × tax rate

= $155,000 × 40%

= $62,000

Now, the journal entry would be:

Income tax expense A/c Dr $84,000

To Income tax payable $62,000

To Deferred tax liability $22,000

(Being income tax expense recorded)

The remaining amount has come under deferred tax liability.

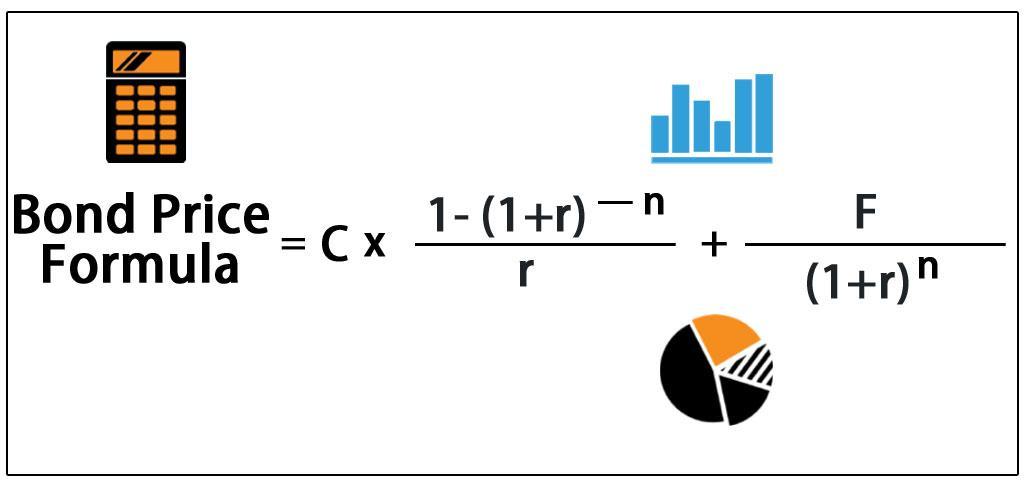

Answer:

Bond Price or Present value = $1196.362948 rounded off to $1196.36

Explanation:

To calculate the quote/price of the bond today, which is the present value of the bond, we will use the formula for the price of the bond. As the bond is an annual bond, the annual coupon payment, number of periods and annual YTM will be,

Coupon Payment (C) = 1000 * 0.1 = $100

Total periods (n) = 20

r or YTM = 0.08 or 8%

The formula to calculate the price of the bonds today is attached.

Bond Price = 100 * [( 1 - (1+0.08)^-20) / 0.08] + 1000 / (1+0.08)^20

Bond Price or Present value = $1196.362948 rounded off to $1196.36

Answer: Financial Intermediation.

Explanation:

Financial Intermediation is a method of wealth distribution common to Banks, where money deposited by it's customers is given out as loan to investors/individuals. The Banks are known as Financial Intermediaries as they are actively involved in wealth distribution.

Answer:

A) Social factor will work for Prince Sports as people are more enlightened not in 21st century

Economic will work for Prince Sports 21st century because manufacturing of sport facilities and equipments are easily produced and better now, infrastructure and development will help improve Prince Sports returns. Technological will work for Prince Sports because technology is simply an improved ways of doing things and with innovation in technology, Prince Sports would be able to solved the contradiction between racquet speed and sweet spot.

Competitive will work for Prince Sports this is because with an increased competition in the of tennis sporting goods companies, Prince Sports would be force to make their brand stand out by rebranding and doing more research on their products improvement.

Regulatory Because of the regulatory forces, the Prince Sports business is governed and everything follows rules and regulations, it has helped Prince Sport to abide by the international regulation laws and prevent the local market of tennis racquets to suffer due to the trade regulations on products.

B) Worked against:

Social: At this age of Social media, people easily give of false information deliberately or unintentionally that tends to misleads customers, which works against Prince Sports.

Competition can make prince sports dwindle of they do not opt their own business

Explanation: