Answer:

Jone Manufacturing

Total Overhead Variance = $2,000U.

Explanation:

Variance is the difference between budgeted and actual expense. It is favorable when the actual is less than the budgeted amount. It is unfavorable when the actual is more than the budgeted amount. It is neither favorable nor unfavorable when the actual equals the budgeted amount.

Variance analysis as a budgeting tool is used to evaluate the performance of management in managing costs, relative to the activity levels.

In Jones Manufacturing, actual and budgeted costs are calculated as follows:

Actual costs:

Fixed overhead = $8,000

Variable overhead = $4,600

Total = $12,600

Budget costs:

Fixed overhead = $10,000 (2,000 hours x $5)

Variable overhead = $4,600

Total = $14,600

Variance = budgeted overhead minus actual overhead

= $14,600 - $12,600 = $2,000U

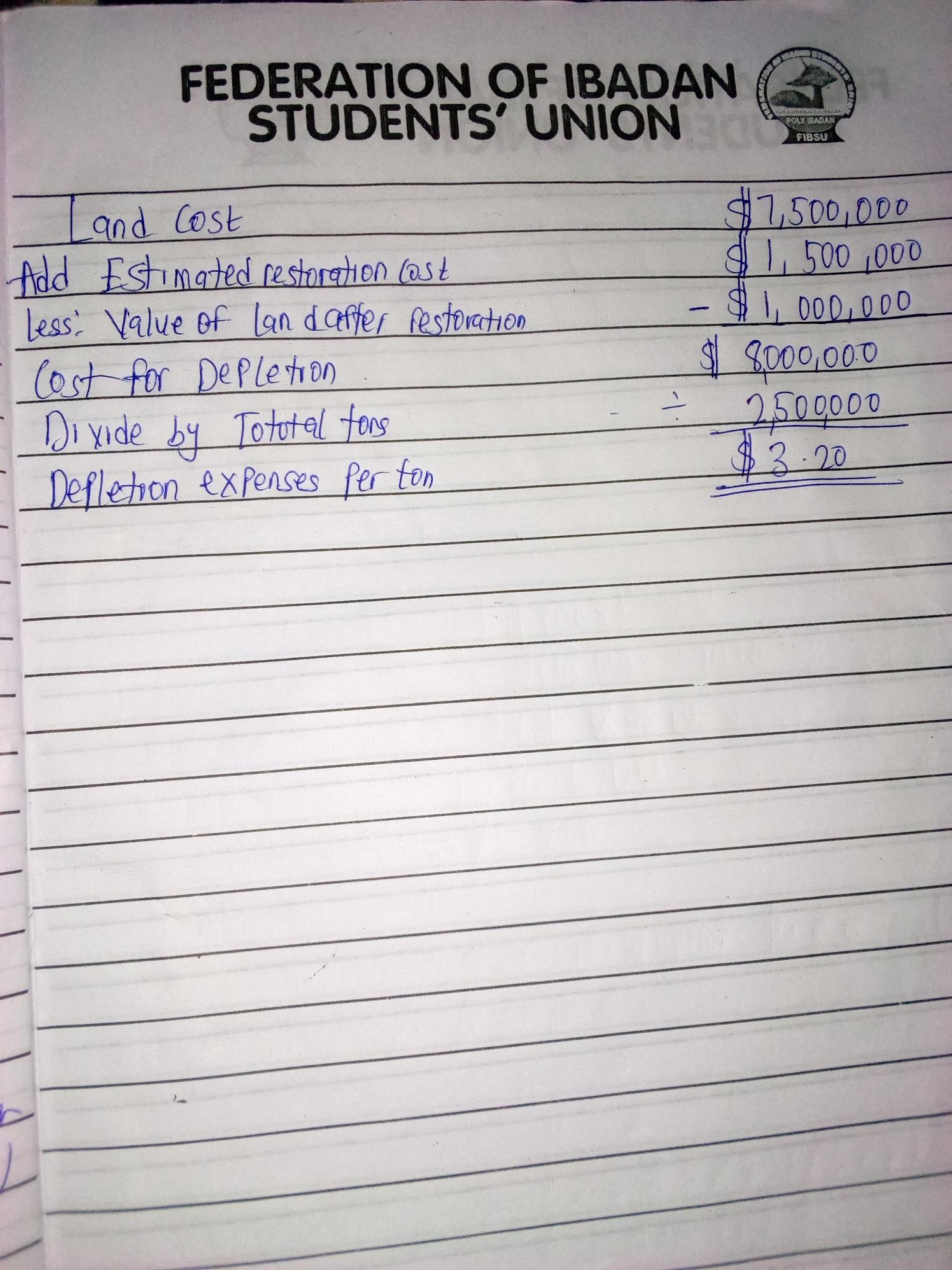

Answer:

$3.20

Explanation:

Kindly check attached picture for explanation

Answer:

$358,150

Explanation:

Cost of goods manufactured is calculated in a Schedule of Manufacturing Costs as follows :

Cost of goods manufactured = Beginning Work In Process + Total Manufacturing Costs - Ending Work In Process

where,

Total Manufacturing Costs :

Materials used in product $124,260

Depreciation on plant $69,650

Property taxes on plant $21,750

Labor costs of assembly-line $120,570

Factory supplies used $25,810

Total $362,040

therefore,

Cost of goods manufactured = $13,700 + $362,040 - $17,590 = $358,150

Answer: $88,400

Explanation:

My corporation Plc

Corporate tax for the year

Operating incom $250,000

Interest received $10,000

Interest paid ($45,000)

Dividends received $6,000

Taxable income $221,000

Since the tax rate is 40%

Tax= 0.4x($221,000) = $88,400.

NOTES

Taxable income is (250000+10000+6000-45000)

Interest paid is in bracket because it's a deduction.

70% of dividends received is excepted from tax

0.3x20000=$6000

Dividends paid out is after tax has been deducted.