Answer:

hey bro how old are u

Explanation:

...................................

Answer:

Find attached complete question.

$ 750.10

Explanation:

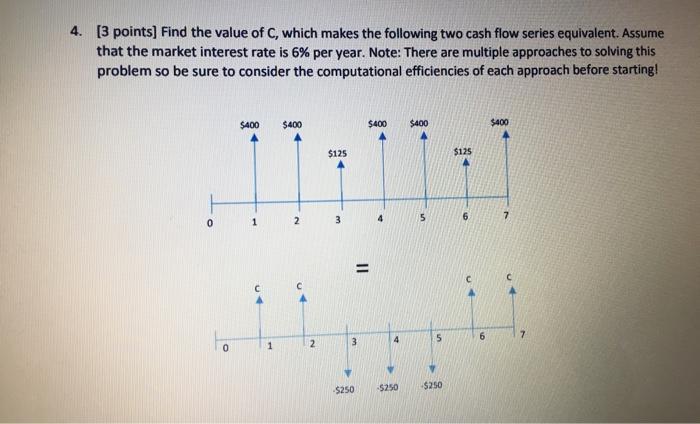

In order to ascertain the value of C ,we need to equate the present value of the two streams of cash flows to each other as follows:

first stream:

$400/(1+6%)^1+$400/(1+6%)^2+$125/(1+6%)^3+$400/(1+6%)^4+$400/(1+6%)^5+$125/(1+6%)^6+$400/(1+6%)^7=$1,808.19

Second stream:

C/(1+6%)^1+C/(1+6%)^2-$250/(1+6%)^3-$250/(1+6%)^4-$250/(1+6%)^5+C/(1+6%)^6+C/(1+6%)^7

-$250/(1+6%)^3-$250/(1+6%)^4-$250/(1+6%)^5=-$594.74

C/(1+6%)^1+C/(1+6%)^2+C/(1+6%)^6+C/(1+6%)^7=C/0.9434+C/0.8900+C/ 0.7050+C/ 0.6651

simplification

C/0.9434+C/0.8900+C/ 0.7050+C/ 0.6651=C/(0.9434+0.8900+0.7050+0.6651)= 0.31216C

All in all:

$1,808.19 =-$594.74+ 0.31216C

$1,808.19+$594.74= 0.31216C

$2402.93

= 0.31216C

C=$2402.93* 0.31216 =$ 750.10

4- your mother buys flour

The Sarbanes-Oxley Act requires both CEOs and CFOs to personally vouch for the reported financial earnings of a company. This law was passed shortly after the Enron scandal.