A.

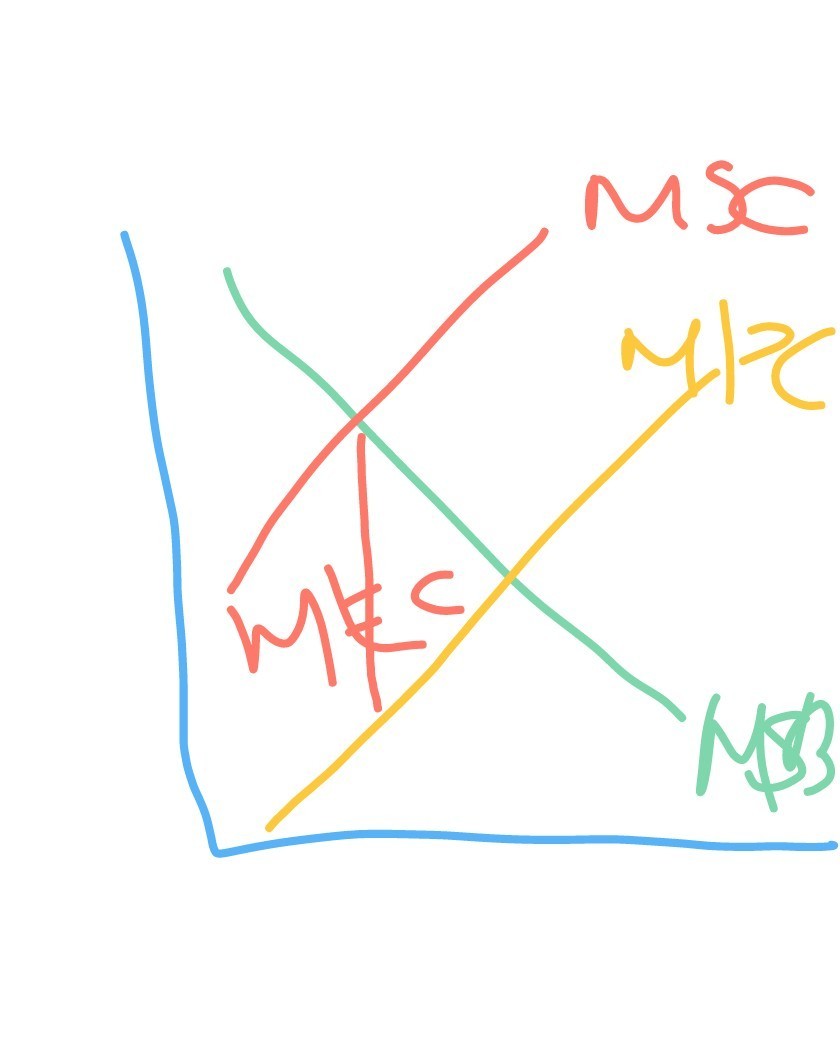

If you recall, negative externalities arise when there is a divergence between marginal private cost and marginal social cost, the difference being the marginal external cost as shown from the poorly drawn diagram. If we got rid of the marginal external cost by producing less, then the externality would dissipate.

However, the question is weird as there are no options for compensation. What would rather happen is that whoever has the property rights will be compensated the size of the MEC and there would be social welfare, whereas the question only tackles removing the externality through stopping production.

Answer:

A commercial for the drink SunnyD explains how nutritious it is in comparison to other, more "sugary" drinks. While children under 12 are the most likely consumers of SunnyD, the commercial is aimed at mothers. These mothers represent SunnyD's target market.

Explanation:

Marketing is a way in which the producer can provide information about it's goods and service to the customers. The marketing channels can either be direct or indirect depending on which strategy works best for the company. The major reason for marketing is to provide more information about the product and services to cover a larger audience. There is always potential in marketing to convert an audience to a loyal customers depending on the effectiveness of the marketing strategy. More customers usually translates to an increase in sales, and ultimately to an increase in profits. Increased profits is a reflection on business success since most companies get into competitive business to make profits. An example of marketing strategy that is often is used is target marketing.

Target marketing is a type of communication with your potential customers that involves providing more information to a select group of people in the market. This is done by tailoring the message in such a way to ensure that it is directed towards that particular group of people. In the question above, the commercial is made in a certain way to target mothers and possibly convert them to loyal customers.

Answer: groupthink

Explanation:

Following the information given in the question, it can be deduced that Steve is being adversely influenced by groupthink.

Groupthink is when a group of people reach a consensus and agree on a particular thing without thinking about other alternatives or the consequences. Groupthink is typically based on the desire not to upset others. In this case, Steve doesn't want to upset and dispute the claims of others.

The last step in making a personal budget is to reduce expenses in flexible categories. The correct option among all the options given in the question is option "B". Under normal circumstances, a person cannot make the adding up all sources of income as the last step. Then the expenses will not get added. The flexible expenses are expenses that can always be reduce or are not important expenses. The basis of making the budget is to reduce those unnecessary expenses. So the last step should always be to find ways to reduce the flexible or unwanted expenses.

<u>The vertical analysis</u> identifies the relative contribution made by each financial statement line item.

<h3><u>Vertical Analysis: What Is It?</u></h3>

Each line item is provided as a percentage of a base figure in the statement as part of a technique called vertical analysis for financial statement analysis. As a result, line items on an income statement and balance sheet can both be expressed as a percentage of gross sales, a percentage of total assets or liabilities, and a percentage of total assets or liabilities, respectively. Vertical analysis of a cash flow statement also displays each cash inflow or outflow as a percentage of total cash inflows.

Learn more about financial statements with the help of the given link:

brainly.com/question/14506917

#SPJ4