Answer and Explanation:

According to the scenario, computation of the given data are as follow:-

1) Semiannually Rate of interest = 11% ÷ 2 = 5.50% = 0.055

Number of years (half yearly) = 4 × 2 = 8 years

PVIF Value = 1 ÷ (1 + Interest Rate)^Number of years

=1 ÷ (1 + 0.055)^8

= 1 ÷ 1.5347

= 0.65160

PVIFA Value = [1 -1 ÷ (1 + Interest Rate)^Number of years ÷ Interest Rate

= [1 - 1 ÷ (1 + 0.055)^8] ÷ 0.055

= [1 - 0.65160] ÷ 0.055

= 6.33457

Particular PV table value Multiply Amount ($) PV value

Principle value 0.65160 × 640,000 $417,024

Annually interest Value 6.33 × 32,000 $202,706

($640,000 × 6 ÷ 12 × 10%)

Present Bond’s Price $619,730

2).

Journal Entry

On Jan.1,2021

Cash A/c Dr. $619,730

Discounts on bond payable A/c Dr. $20,270

To Bond payable A/c $640,000

(Being bond issued at discount is recorded)

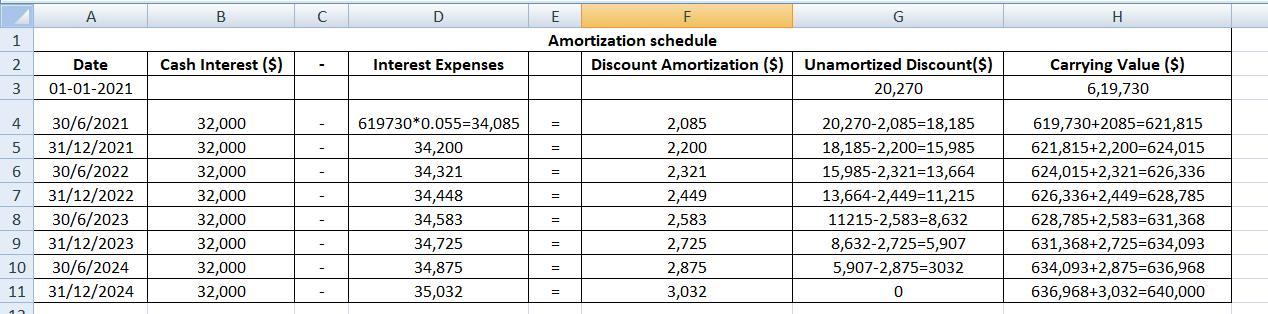

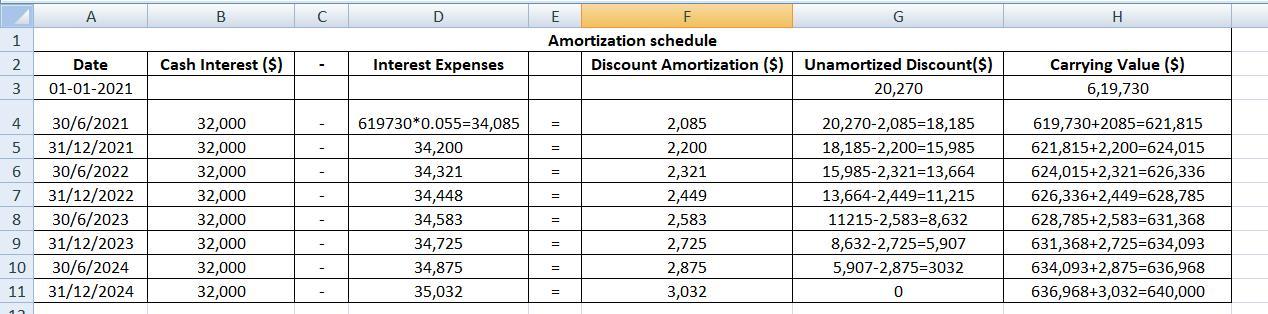

3. The amortizable schedule is presented on the attachment below

4).

Journal Entry

June 30,2021

Interest expense A/c Dr. $34,085

To Cash A/c $32,000

To Discount on bond payable A/c $2,085

(Being interest expenses is recorded)

5) On December 31,2021 Amount of bonds reported = $624,015

6). Interest expenses reported in income statement

= $34,085 + $34,200

= $68,285

7).

Journal Entry

On Dec. 31,2024

Interest expense A/c Dr. $35,032

To Cash A/c $32,000

To Discount on bond payable A/c $3,032

(Being interest expense is recorded)

On Dec.31,2024

Bond payable A/c Dr. $640,000

To Cash A/c $640,000

(Being interest expense is recorded)