first look at the starting value then approximately affect the ending value

Answer: Check attachment

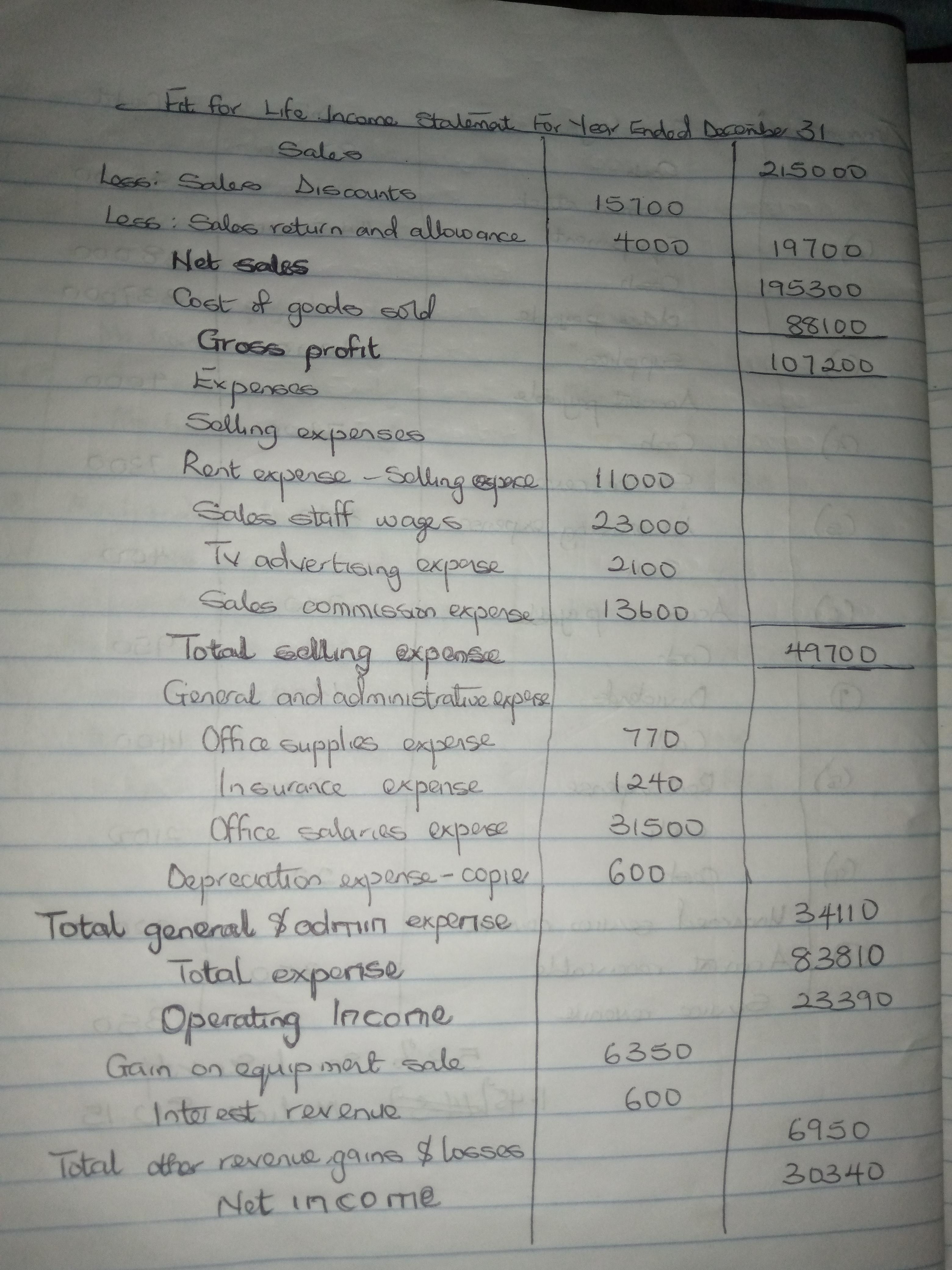

Explanation:

Note that, in the attachment, the total expense was calculated as the addition of the selling expense and the general and administrative expenses. This will be:

= $49700 + $34110

= $83810

Operating income was calculated as:

= Gross profit - Total expenses

= $107200 - $83810

= $23390

Check the attachment for further details.

Explanation:

The administration course contributed with several essential concepts for the work and career of every professional.

In my opinion, the two most important concepts learned in this course were the development of marketing plans and management of social media.

Learning about the strategic importance of implementing a marketing plan will help the professional to understand the crucial steps in the development of the product and its phases until reaching the end customer. Another essential learning was social media, which is a worldwide trend in building customer and company relationships and cannot be ignored nowadays, through this new channel companies are able to establish a relationship marketing capable of creating value for the brand and increasing customer loyalty.

Workers who are known to have skills to operate machines and who only require a minimum amount of training are semiskilled laborers. They are known as semiskilled due to the fact that they work using a bit of skills only, and they don't require to learn the whole aspects of the machine.

Answer:

B. people respond to economic incentives.

Explanation:

Economic incentive is material given by someone, that is capable of motivating the other person to behave or act in a certain way. If economic incentives come from a government, it can be in form of tax incentives, subsidies or any monetary gift in form of cash or near cash.

To the economist, human being being rational, will respond to economic incentives in various forms.