Answer:

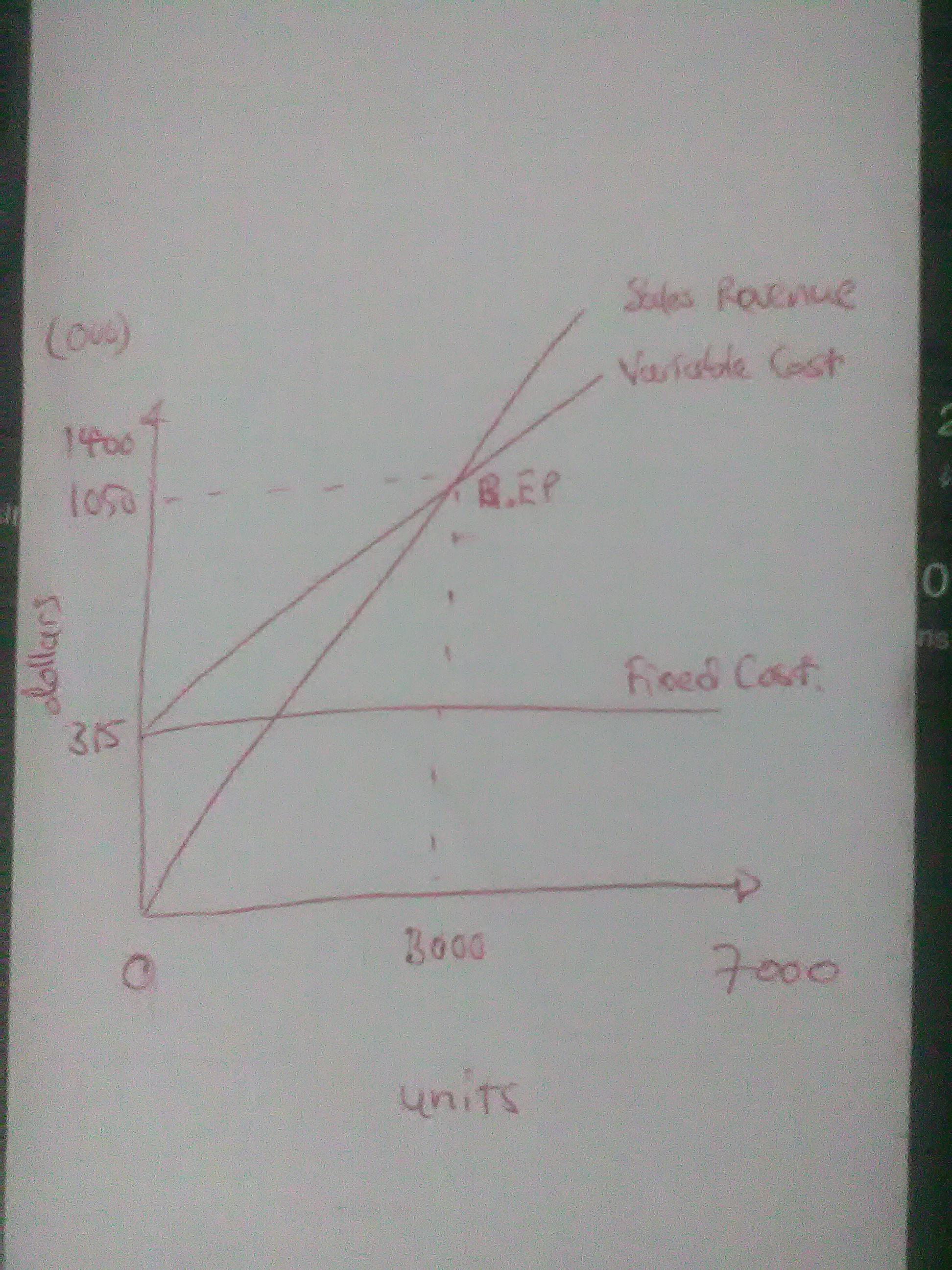

1a. 3,000 units

1b. $1,050,000

2. See attachment.

3. contribution margin income statement

Sales ($350 × 7,000 units) $2,450,000

Less Variable Cost ($245 × 7,000 units)) ($1,715,000)

Contribution $735,000

Less Fixed Costs ( $315,000)

Operating Profit $420,000

Explanation:

Break-even point (sales units ) = Fixed Cost ÷ Contribution per unit

= $315,000 ÷ ($350 - $245)

= 3,000

Break-even point (sales dollars) = Fixed Cost ÷ Contribution Margin Ratio

= $315,000 ÷ ($105/$350)

= $1,050,000

Draw up a monthly budget. A monthly budget can do wonders for managing your month-to-month living expenses

<h2>Real-time analytics is the technology used by online stores to present customized content.</h2>

Explanation:

Real-time analytics is the,

- combination of "Mathematics and logic"

- Analysis of date

- Enables business to react without any delay

- User can draw conclusion within a short span of time

- Provides insights of collected data

- To maximize the satisfaction of the customer

- To maximize the business by informing about promotion of the product

- Enables business to immediately react to data

Example:

- viewing orders that the customer has made

- Updating of cart

Answer:

The statement that is not correct is:

- <u><em>B) A purchase of equipment is classified as a cash outflow from investing activitites.</em></u>

Explanation:

<u><em>A) Paying dividends to investors creates a cash outflow from financing activities. </em></u>

This is correct.

The financing cash flow or cash flow generated by financing activities is the cash flow that involves transactions with the banks (only the long term debt) or stake holders: financing debt, equity, and dividend.

Issuing equity of debt is a cash inflow: increases the cash of the company.

Paying dividends, such as repurchasing debt or equity are cash outlfow: decreases the cash of the company.

<u><em>B) A purchase of equipment is classified as a cash outflow from investing activities.</em></u>

<u><em></em></u>

This is not correct.

The operating cash flow is the cash that involves the operations of the company: sales (revenue), trade receivables, operating investement in building and equipments used for the operation, purchases from suppliers (inventory).

When you purchase an equipment it diminishes the cash or impact an operating account; thus, a purchase of equipment is classified as a cash ouflow from operating activities, not from investing activities.