Answer:

C. There should be logical association between the allocation base and the incidence of costs.

Explanation:

We define the allocation base as that quantity through which the overhead cost and be allocated to. This base is usually in the form of a quantity. It could be the kilowatts used in hours, or the machine hours used.

It should be able to show to a logical extent how the cost object used the resources to which it is assigned

A firm that wanted to enable its employees to use and share data without allowing outsiders to gain access could do so by establishing a: intranet

This is further explained below.

<h3>What is an intranet?</h3>

Generally, A company that intended to provide its workers the ability to utilize and exchange data while preventing unauthorized third parties from gaining access to such data may do so by building an intranet.

In conclusion, a private network built using World Wide Web technologies; is a local or limited communications network.

Read more about the intranet

brainly.com/question/19339846

#SPJ1

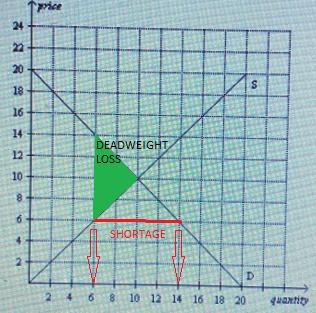

Answer:

A price ceiling set at $6 will be binding and will result in a shortage of 8 units.

Explanation:

In order for a price ceiling to be binding, it must be set below the equilibrium price level. In this case, $6 is below the equilibrium price of $10. It will produce a shortage of 8 units because the quantity supplied by producers will be only 6 units, while the quantity demanded by consumers will be 14 units.

Binding price ceilings always produce a deadweight loss which is represented by the area between the demand curve and the supply curve left to the equilibrium price.

Explanation:

On the books of Shore Co

Cash A/c Dr $111,560

Sales discount A/c $2,240 ($11,2000 x 2%)

To Accounts receivable A/c $113,800 ($112,000 + $1,800)

(Being cash is received)

On the books of Blue star

Accounts payable A/c Dr $113,800 ($112,000 + $1,800)

To Merchandise inventory A/c $2,240 ($11,2000 x 2%)

To Cash A/c $111,560

(Being cash is paid)

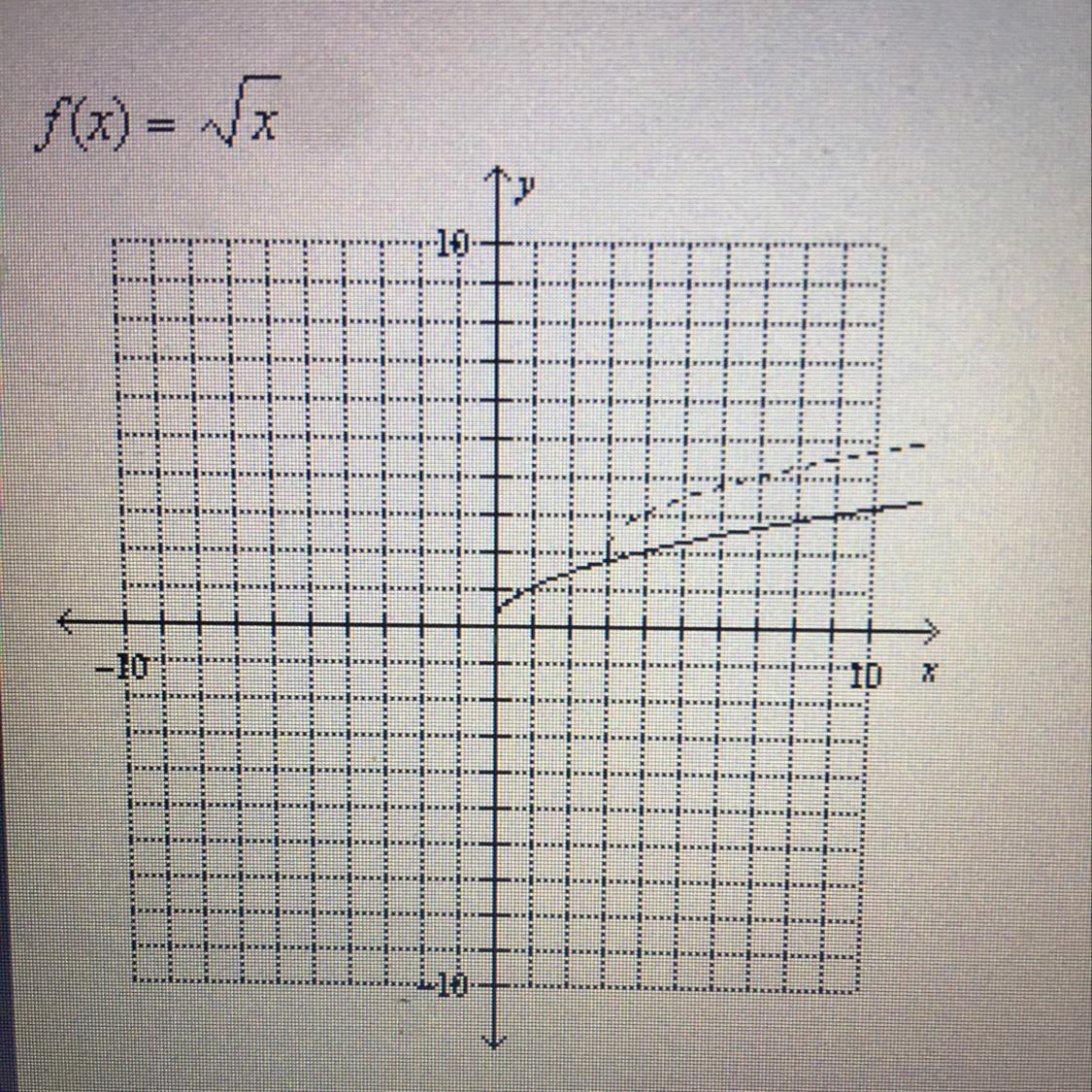

Answer:

<em>Translate the parent function, 2 units upward</em>

Step-by-step explanation:

Given

See attachment for the graph

Required

Determine the change in f(x) that gives the dashed line

Let the dash line be represented with g(x)

From the attachment, there is only one transformation from f(x) to the g(x).

When f(x) is translated 2 units vertically upwards

, it gives g(x); the dash line.

If

Then g(x) is: