To resolve a problem or select between multiple options

Answer:

Effect on income= $115,000 decrease

Explanation:

Giving the following information:

Fixed costs= $45,000

Number of units= 20,000

Unitary contribution margin= $8

<u>To calculate the effect on income, we need to use the following formula:</u>

Effect on income= decrease in fixed costs - decrease in contribution margin

Effect on income= 45,000 - 20,000*8

Effect on income= $115,000 decrease

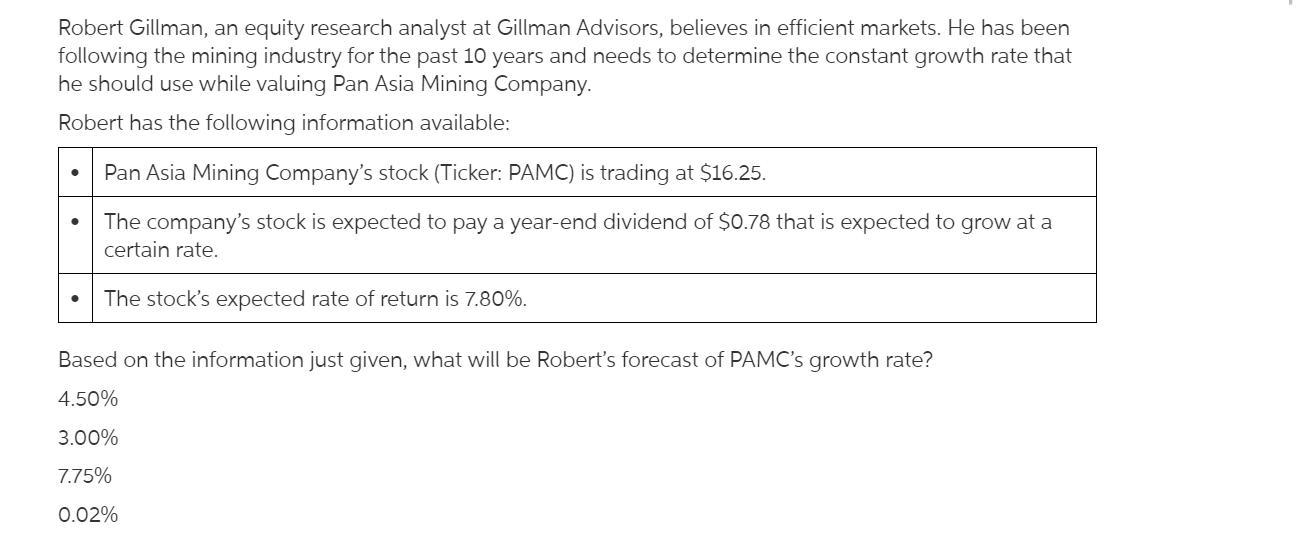

Answer:

the growth rate is 3%

Explanation:

The computation of the PAMC growth rate is shown below:

Price of the stock = Current year dividend ÷ (required rate of return - growth rate)

$16.25 = $0.78 ÷ (0.078 - growth rate)

0.078 - growth rate = 0.048

So, the growth rate is 3%

We simply applied the above formula so that the correct value could come

And, the same is to be considered

Answer:

The answer is 6.151%

Explanation:

The weighted average cost of capital (WACC) of the project is also the internal rate of return (IRR). The IRR formula is calculated by equating the sum of the present value of future cash flow less the initial investment to zero.

Answer: Option (A) is correct.

Explanation:

Here, it's given that the shareholders believe jets be utilized for purposes which are in accordance with increasing the profits of Company G.

From the given comprehension the following must be true in order to support the reason behind shareholders' objection: <em>Company G executives usually utilize corporate jets for personal travel. </em>

Since utilizing organizations's corporate jet for private use won't increase it's profit. This explains why the shareholders had an objection to executives' use of the corporate jets.