Commonly used in accounting analysis, a <u>Financial Ratio </u>shows a relationship between two elements of a firm's financial statements

A financial ratio is a measure of the relationship between two or more components of a company's financial statements. These metrics provide a quick and easy way to track performance, benchmark against industry peers, identify problems, and proactively implement solutions.

They are primarily used by outside analysts to determine various aspects of the company, such as B. Profitability, liquidity, and solvency.

a financial ratio is divided into five types: liquidity metrics, leveraged financial metrics, efficiency metrics, profitability metrics, and market valuation metrics.

Disclaimer: Learn more about financial ratios here brainly.com/question/21631170

#SPJ4

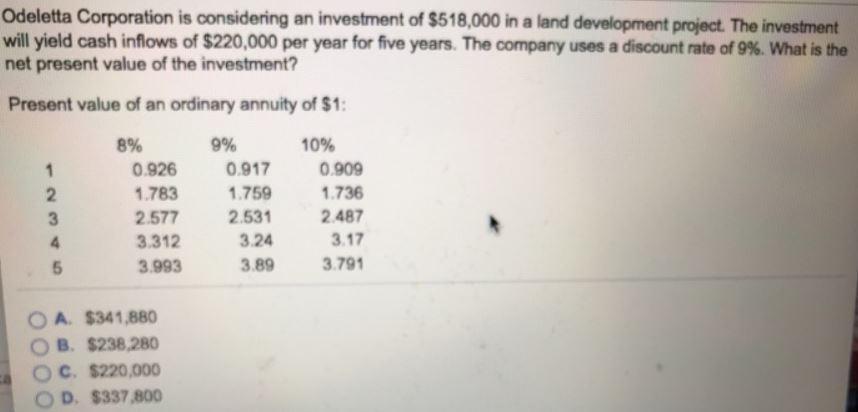

Answer: $337,800

Explanation:

Cashflow is constant so is an annuity.

The Present value of the Investment;

= Present Value of Cashflow - Investment cost

= (220,000 * Present value interest factor of an annuity, 5 years, 9% ) - 518,000

= (220,000 * 3.89) - 518,000

= 855,800 - 518,000

= $337,800

Answer:

$ 5000

Explanation:

Economic Profit = Revenue - Cost of Material - Opportunity Cost

Economic Profit = 50,000-20,000-25,000

Economic Profit = $5000

Answer:

A.) Medium of exchange - Here money is used for doing transaction and therefore, this example is under the medium of exchange.

B.) Store of value - Here, a person store or deposits his money into a bank and therefore, this shows the store of value characteristic of money.

C.) Medium of exchange - Here, one of my friend utilize money for helping me mowing lawns which shows that money is used as a medium of exchange.

D.) Unit of account - The unit of account characteristic of money is reflected here because a person easily calculated his net earnings for the year on the tax return in terms of money.

E.) Unit of account - The unit of account characteristic of money is reflected here because a person easily calculated his new lawn mower value.