The cost of unloading is $52,000

Explanation:

Cost is the cash interest that a corporation has expended on sales and accounting to manufacture it. Within an organization, costs represent the amount of money spent on manufacturing or developing a good or service. Price requires no benefit premium.

Resource Unloading Equipment $15,000

Fuel $2,000

Operating Labour = (25% × [4 $35,000] = $35,000)

= $35,000

Total = $35,000+$15,000

+$2,000

= $52,000

Option C wearing straw hats become popular

Answer and Explanation:

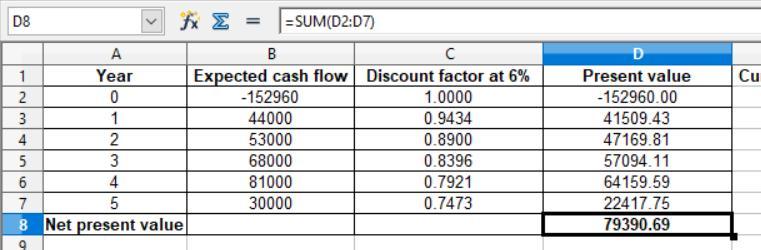

The computation of the net present value is presented in the attachment below:

For project A, the net present value is $91,771.53 and for project B, the net present value is $79,390.69

It is computed after considering the discounting factor that comes from

= 1 ÷ (1 + discount rate)^number of years

for year 1, it is

= 1 ÷ (1 + 0.06)^1

The same applied for the remaining years

Answer:

(B) a cash cow

Explanation:

Based on the information provided within the question it can be said that in this scenario AI Rubber would be considered a cash cow. This term refers to a business and/or product that generates a steady revenue or profit for the owning company or individual. Since AI Rubber has a 45% market share we can say that they are the cash cow of the corporation.

Answer:

$6.30

Explanation:

For computing the unit price, first we have to determine the difference in cost which is shown below:

= $150,000 - $120,000

= $30,000

Now the break even price would be

= Variable cost + cost difference

= $600,000 + $30,000

= $630,000

So, the unit price would be

= Break even price ÷ number of unit produced

= $630,000 ÷ 100,000 units

= $6.30