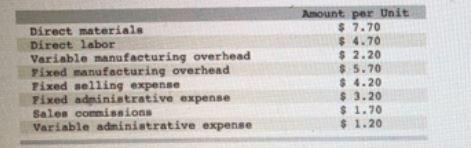

Based on the details given, the following are true:

- 1. Incremental manufacturing cost = $14.60

- 2. Incremental cost = $17.50

<h3>Incremental manufacturing cost if production increased from 20,250 to 20,251</h3>

The fixed cost will not change as the production amount is still below 24,500 units. Incremental manufacturing cost will therefore be:

= Direct material + Direct labor + Variable overhead

= 7.70 + 4.70 + 2.20

= $14.60

<h3>Incremental cost for increased from 20,250 to 20,251</h3>

This will include all costs that are not fixed.

= Incremental manufacturing cost + Sales commissions + Variable admin expense

= 14.60 + 1.70 + 1.20

= $17.50

Find out more on incremental manufacturing cost at brainly.com/question/8527680.

Answer:

The Intrinsic value is calculated by multiplying the Earnings per share by the P/E ratio.

1. The lowest P/E ratio is 21.37 so the intrinsic value is;

Intrinsic value = 2.1 * 21.37

= $44.88

2. Highest P/E ratio is 23.49

Intrinsic value = 2.1 * 23.49

= $49.33

3. The average P/E ratio is;

= (22.07 + 23.49 + 21.37)/3

= 22.31

Intrinsic value = 2.1 * 22.31

= $46.85

Assets that are not expected to provide benefits for a number of accounting periods are called b. fixed assets

Answer: It just would not be a cross walk it would be a road.

Explanation:

The Last-In, First-Out (LIFO) inventory costing method assumes that items in ending inventory are the most recently acquired.

<h3>What is LIFO and FIFO methods of inventory?</h3>

LIFO refers to the Last In, First Out. LIFO is a method that assumes that the last unit that has been added in the inventory or more recently, will be sold first.

FIFO stands for First In, First Out. FIFO method assumes that the oldest unit of inventory that has been added first, would be sold first.

Basically, FIFO and LIFO accounting are the inventory costing methods used in managing inventory.

Learn more about LIFO and FIFO here:-

brainly.com/question/17236535

#SPJ4