Answer: D) Output decreases by more than 25 percent

Explanation:

When a firm is said to be experiencing Increasing Returns to Scale, it means that for every additional unit of a factor of production, the firm experiences a higher increase in production than the additional unit. For example, if a Firm's output increases by 1.5 every time they hire an extra worker, the firm is said to be going through Increasing Returns to Scale.

With that same logic, if factors of production were reduced, the company undergoes a reduction in output that is bigger than the reduction in the factor of production.

For this reason, option D is correct in saying that Output decreases by more than 25 percent.

Answer:

Next year's annual dividend divided by today's stock price

Explanation:

Dividend yield is a financial ratio which is used by investors to assess a company's annual dividend payout in comparison of its stock price. The formula for dividend yield ratio is :

Annual dividend / Stock price

The annual dividend used is the most recent dividend paid or is to be paid to shareholders of the company. It enables investors to assess the return on their investment in each stock price. Dividend yield increases when companies pay more dividends. It is a good signaling effect for shareholders.

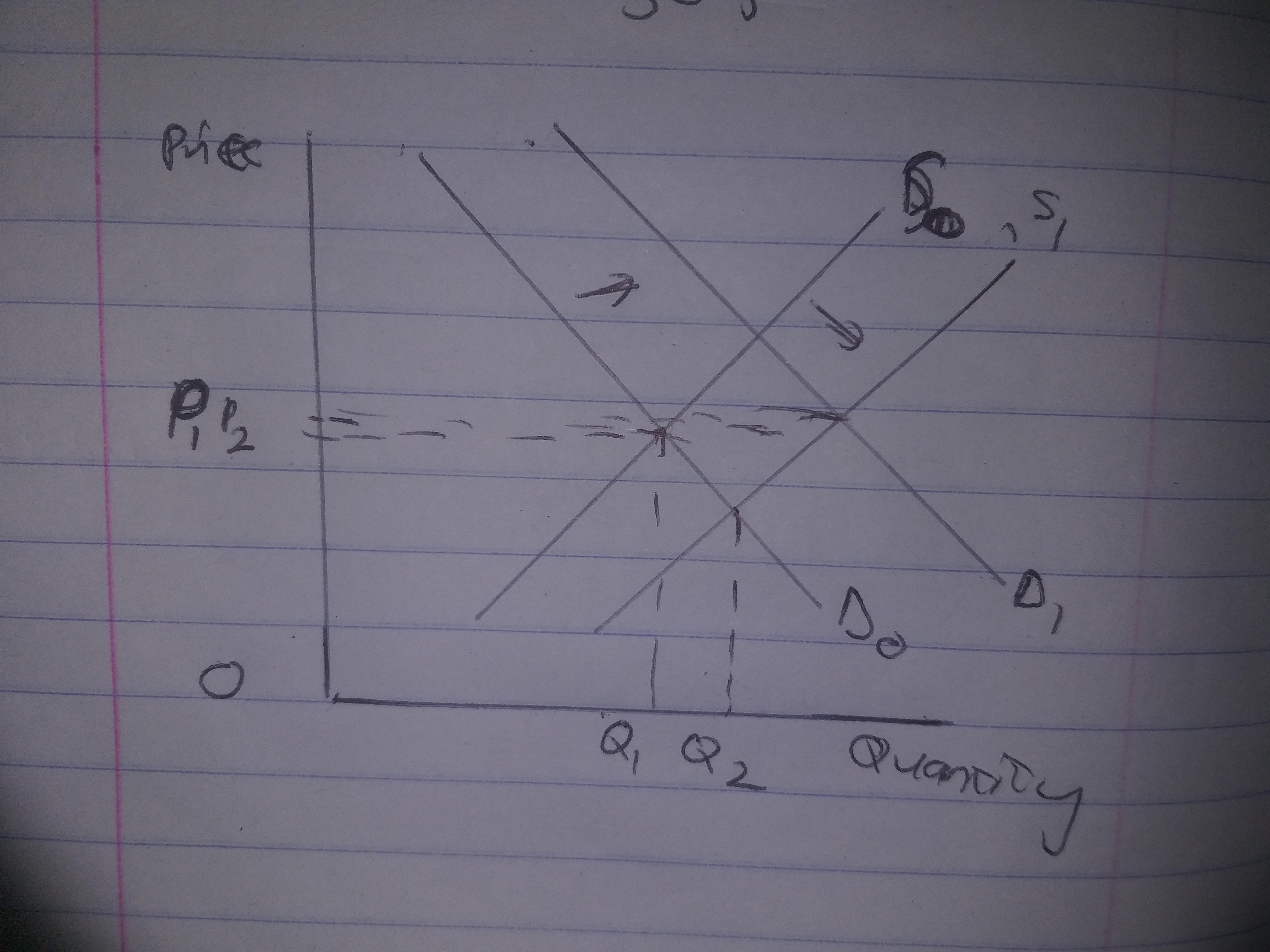

Answer:

there would be a rise in equilibrium quantity and an indeterminate effect on equilibrium price

Explanation:

as a result of the scientists revelation, the demand for oranges would increase and so would the price.

as a result of the new fertilisers been used, the supply of oranges would rise and price would fall.

taking these two occurrences together, there would be a rise in equilibrium quantity and an indeterminate effect on equilibrium price

There will be a formal on-boarding process for all new employee so as to learn the structure and culture of the organization for a standardized process.

<h3>Why is the onboarding process is necessary for new employees?</h3>

"Onboarding processes is required in an organization so as to help the new employee to be able to be fully integrated into the organization.

This will help to prevent or get rid of complaints of the customer about employee not knowing the culture and way of doing things in the organization.

learn more about Onboarding at brainly.com/question/24448358

#SPJ1

Answer:

Explanation:

Initiation phase is the first phase of a project management where the project is evaluated to know the purposes it has to be done , how it will be done and the resources needed to execute it.

At this stage , Samantha's team has to clarify and justify the project's purposes and feasibility in order to know why it has to be done and also how it will be completed and its purpose achieved.