Answer:

$1,000

Explanation:

No fault insurance basically protects you and your family from small accidents by paying your medical bills regardless of who is at fault. This type of policies applies to car or house insurance.

In this case, the accident was caused by Jason but since who is responsible is not important in this type of policy, then it should cover up to its maximum limit.

Answer:

Explanation:

knowledge? Sorry if this dosent help! <3

Answer:

The answer is D) will raise disposable income and raise spending

Explanation:

When taxes are cut disposable income increases as there is less income used to pay taxes. If there is a higher amount of disposable income available then spending will increase as well as spending appetite.

Cutting taxes is a easy way to stimulate spending in an economy.

The correct answer is therefore D) will raise disposable income and raise spending.

Cutting taxes can also increase aggregate demand which can lead to higher economic growth as well.

Answer:

In a large open economy, if political instability abroad lowers the net capital outflow function, then the real interest rate falls, while the real exchange rate rises and net exports fall. (D)

Explanation:

NX = EXPORTS – IMPORTS

If political instability abroad lowers the net capital outflow function that would mean that NX is reducing, which increasing imports and decreasing exports. This means that domestic goods are relatively more expensive due to a high exchange rate. In terms of the real interest rate, it falls because the demand for financial assets decreases.

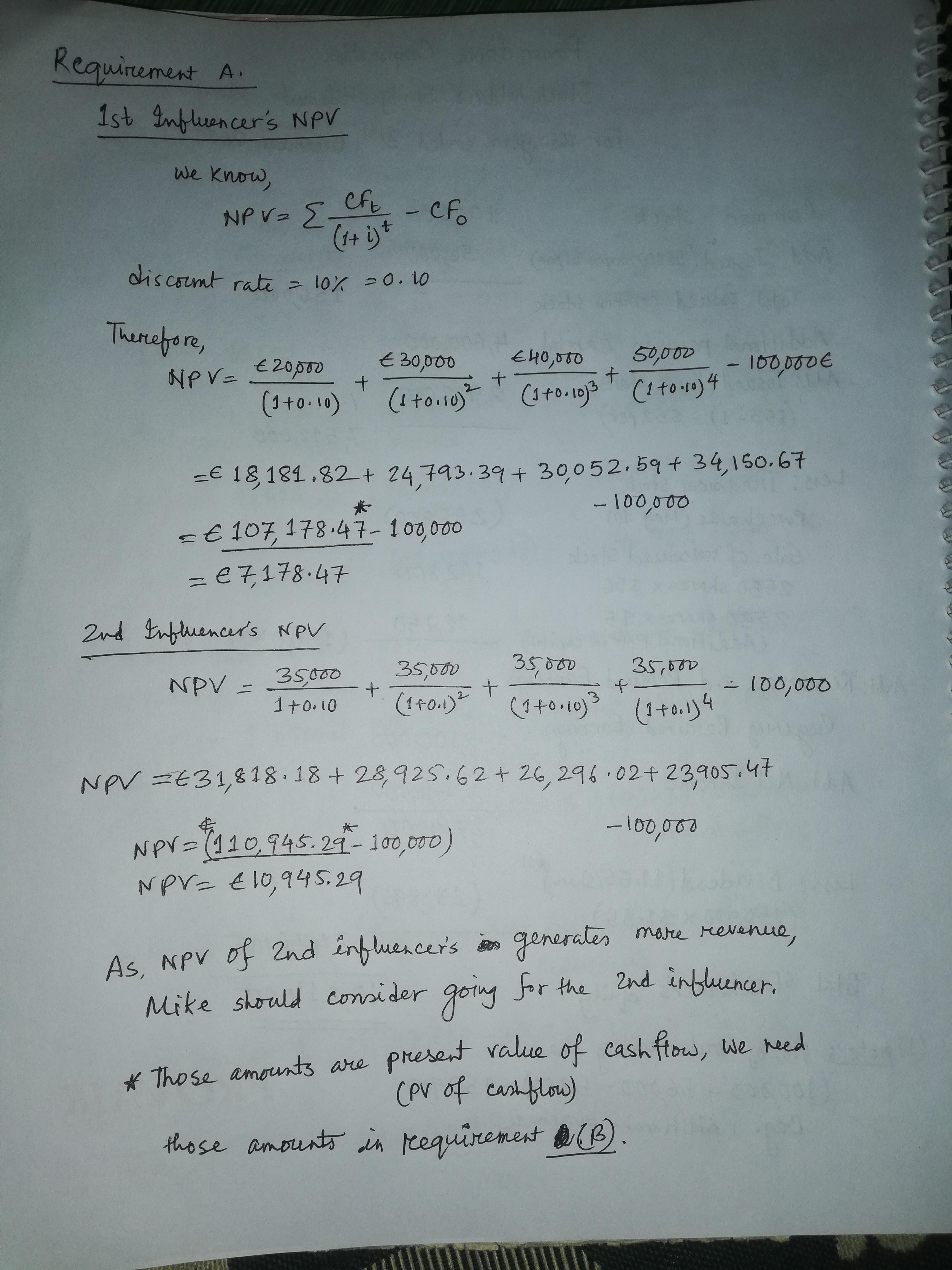

Answer:

A) Based on NPV, Mike will choose 2nd influencer.

B) Based on IRR, Mike will choose 2nd influencer.

Explanation:

See images to get the appropriate answer: