The answer is <span>allowed physical ability tests to be given to applicants if the tests are job-related.

It provided Americans with disabilities to have job opportunity on a skill they have that can match jobs that are needed by a company. It also helps the company find and help them have a job which they can do. It benefited both the company and the employee.</span>

You did not post the complete question so I will write only the missing components below that is needed to answer the question and some important definitions.

Definitions:

PVIFA - present value interest factor of annuity

= number of regular intervals per year at which time the borrowed amount is to be paid back

= number of regular intervals per year at which time the borrowed amount is to be paid back

= annual interest rate

= annual interest rate

= number of years to payoff the debt

= number of years to payoff the debt

We need to find the interest rate that equates the price we paid for the bond with the cash flows we received. The cash flows we received were $100 each year for two years and the price of the bond when we sold it. Also, remember the YTM on the bond has declined by 1 percent.

Let us assume a par value of $1,000. we need to find the price of the bond in two years. The price of the bond in two years, at the new interest rate, will be:

$100(PVIFA8.42%,17) + $1,000(PVIF8.42%,17) = $1,139.69

Answer:

Therefore, the bond will sell for $

1,139.69 ± 0.1%

Answer:

I prepared an amortization schedule using an excel spreadsheet. The original monthly payment was $836.44. After the 120th payment, the remaining principal balance was $68,940.64. Since she didn't pay anything for 1 year, the new principal balance will be $68,940.64 x (1 + 8%) = $74,455.89

I prepared another amortization schedule for the remaining 9 years, and the monthly payment is $969.32. She will pay off the loan in 108 months.

<span class="sg-text sg-text--link sg-text--bold sg-text--link-disabled sg-text--blue-dark">

pdf

</span>

<span class="sg-text sg-text--link sg-text--bold sg-text--link-disabled sg-text--blue-dark">

pdf

</span>

Consumer credit dates back to colonial times.

<h3>What is consumer credit?</h3>

Money that customers can borrow to pay for products or services is known as consumer credit. Customers who have access to credit can make purchases today and pay for them over time. Consumers can obtain credit from banks, financial organizations, and companies.

Consumer credit is governed by federal and state rules that shield borrowers from dishonest lending practices and stop companies from treating them differently based on non-financial considerations.

Examples of consumer credit are credit cards, education loans, mortgages, etc.

Consumer credit has been around since the colonial era when farmers used it frequently.

Learn more about consumer credit here:

brainly.com/question/17237024

#SPJ4

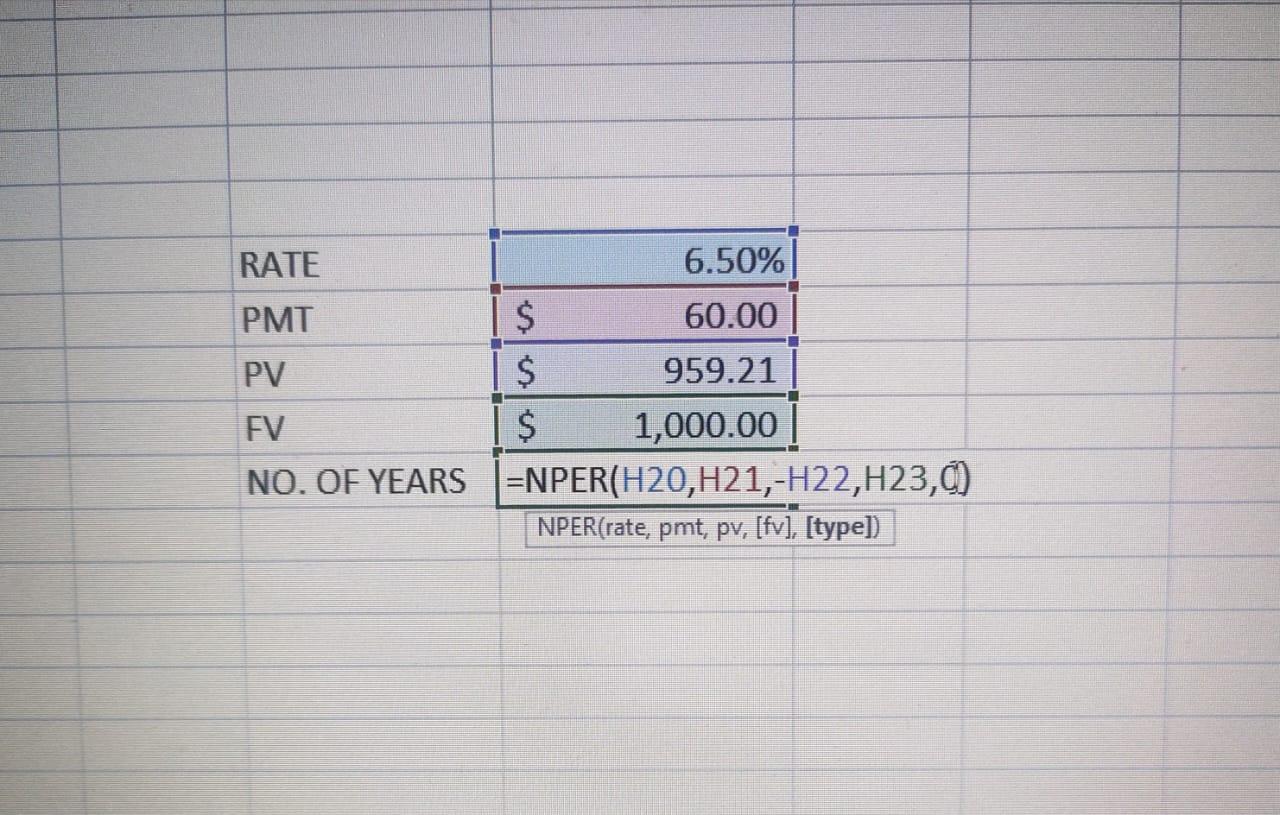

At the current interest rate of 6.5%, the bonds will mature in 12 years.

CALCULATIONS:

RATE= 6.5%

PMT= 1000$*6% = 60$

PV= 959.21$

FV= 1000$

NO. OF YEARS TO MATURE= NPER(rate, pmt, -pv,fv,0)

=NPER(6.5%,60$,-959.21$,1000$,0)

=12 YEARS

A coupon bond, also known as a bearer bond or bond coupon, is a debt obligation that includes semiannual interest coupons. The issuer keeps no record of coupon bond purchasers, and the purchaser's name is not printed on any kind of certificate. Between the time the bond is issued and the time it matures, bondholders receive these coupons.

Coupons are typically described in terms of the coupon rate, which is the yield paid on the date of issuance by a coupon bond. The interest rate on the coupon is subject to change. The coupon rate is calculated by adding all of the annual coupons and dividing the total by the bond's face value.

Learn more about coupon bonds here:

brainly.com/question/14746407

#SPJ4