Answer:

Cp = 1.667

Cpk = 1.25

The filling process will deliver the customer's specifications since Cp > 1 and Cpk > 1

Explanation:

Given data:

Customer Specification 3.98 4.02

Process Average 4.005

Process Standard Deviation 0.004

<u>Calculate the Cp and Cpk values</u>

Cp = Δ customer specification / ( 6 * std )

= (4.02 - 3.98 ) / ( 6 * 0.04 )

= 0.04 / 0.24 = 0.1667 + 1 = 1.667

Cpk ( upper ) = ( 4.02 - process average ) / ( 3* std )

= ( 4.02 - 4.005 ) / ( 3 * 0.004 ) = 1.25

Cpk ( lower ) = ( process average - 3.98 ) / ( 3 * std )

= ( 4.005 - 3.98 ) / ( 3 * 0.04 ) = 2.083

Cpk = minimum value of Cpk = 1.25

Answer:

All the following are advantages of ERP systems except: ______

c. moderate to low cost

Explanation:

Enterprise resource planning (ERP) integrates the important parts of their businesses and reduces the time and efforts required to do work. A good ERP system enables teams to focus on revenue-generating tasks by eliminating repetitive tasks. But, these advantages come at some steep costs, especially in initial infrastructure and continuous maintenance.

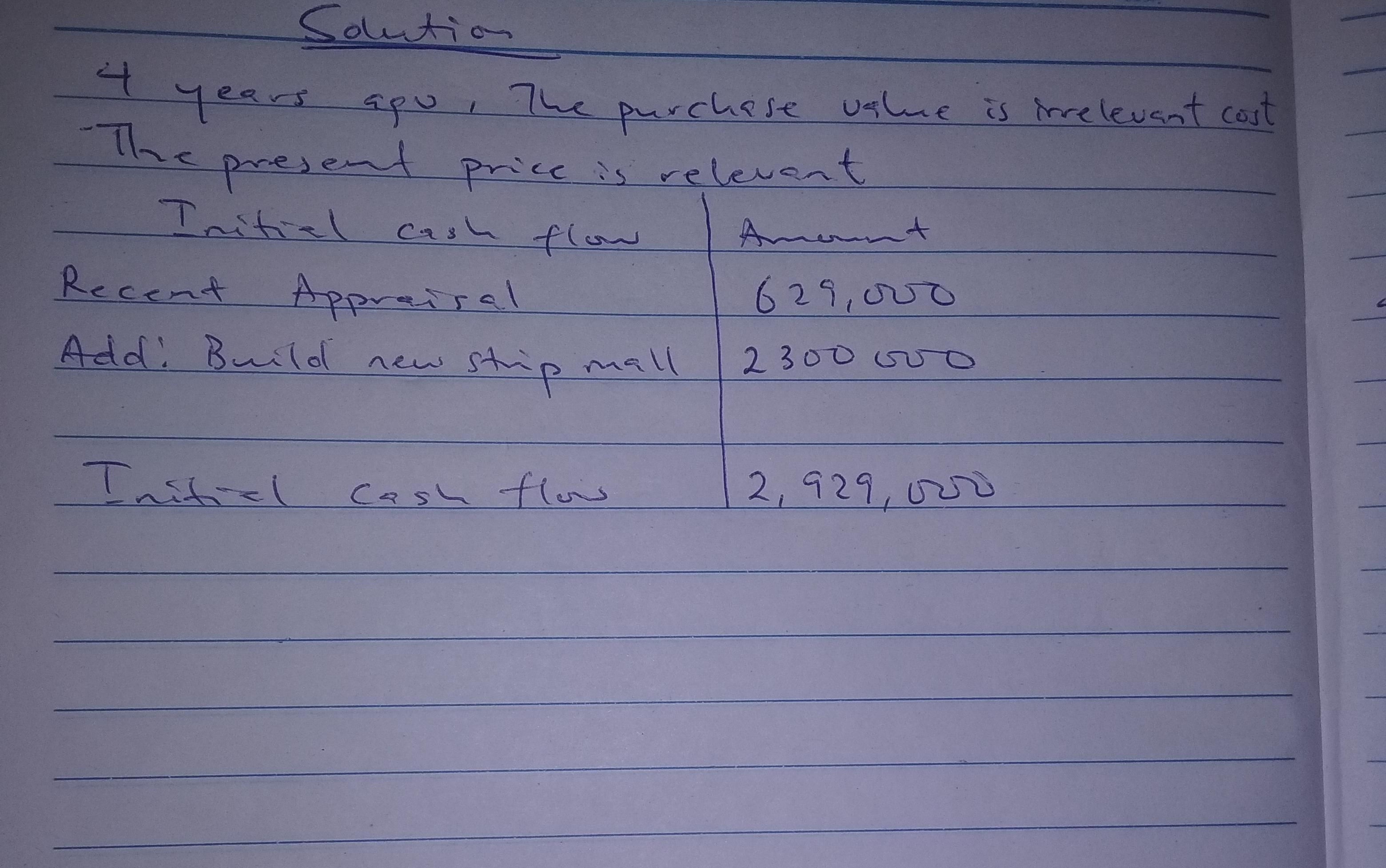

Answer:

initial cash flow is 2,929,000

Explanation:

Attached is the table

Answer: d. 3 years

Explanation: Gender identity is a personal sense of what gender an individual is. It may or may not be the same thing as the gender registered at birth. Before age 3, children hardly notice the differences but at this age, they are aware of their environment and the basic differences between the two genders.

At this age, most children identify as their birth gender as they learn from the environment their gender expectations; from their family, school,religious organisations; and they are aware of the fundamental differences between the genders.

Answer:

the answer is C. a legal entity of people who share a common mission.