The answer is the first one. Demand alludes to the amount of an item or administration is wanted by purchasers. The amount demand is the measure of an item people will purchase at a specific value; the connection amongst cost and amount requested is known as the requested relationship. The law of demand expresses that, if every other factor stays measure up to, the higher the cost of a decent, the fewer individuals will request that great. As such, the higher the value, the lower the amount requested. The measure of a decent that purchasers buy at a higher cost is less in light of the fact that as the cost of a decent goes up, so does the open door cost of purchasing that great.

Answer

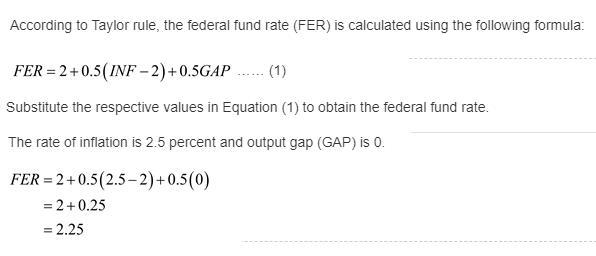

The answer and procedures of the exercise are attached in the following archives.

Explanation

You will find the procedures, formulas or necessary explanations in the archive attached below. If you have any question ask and I will aclare your doubts kindly.

If the price of a product falls to what is considered a bargain price, a shortage would occur.

A shortage occurs when the quantity demanded exceeds the quantity supplied. A shortage occurs when price is below the equilibrium price.

A surplus is when the quantity supplied exceeds the quantity demanded. A surplus occurs when price is above the equilibrium price.

When the price of a good falls to what is considered a bargain price by consumers, it means that the price of the good is below the equilibrium price.

When the price of a good is below equilibrium, quantity supplied would fall and the quantity demanded would exceed supply. As a result, there would be a shortage.

To learn more about shortage, please check: brainly.com/question/16137233?referrer=searchResults

Answer:

$90,000

Explanation:

Sales revenue $350,000

Cost of goods sold $150,000

Operating expenses $110,000

Foreign currency translation gain $25,000

Gross profit= sales revenue - the cost of goods sold

=$350,000-$150,000

=$200,000

Net income = Gross profit - Operating expenses

=$200,000 - $110,000

=$90,000