Answer:

<u>b) The corporation survives even if managers are dismissed.</u>

<u>c) Shareholders can sell their holdings without disrupting the business.</u>

<u>Explanation:</u>

The above statements are correct descriptions of large corporations if consider;

1. A corporation is viewed as a legal entity, and so is believed to exist (survive) even if those who manage the corporation are dismissed.

2. Put simply, a shareholder holds some owns certain decision rights of a corporation, thus, the shareholder can decide to sell their holdings to an interested party. However, the business would not be disrupted, as only the holdings of a particular shareholder were sold, and the new shareholder would normally want the best interest of the company that's why he made the deal.

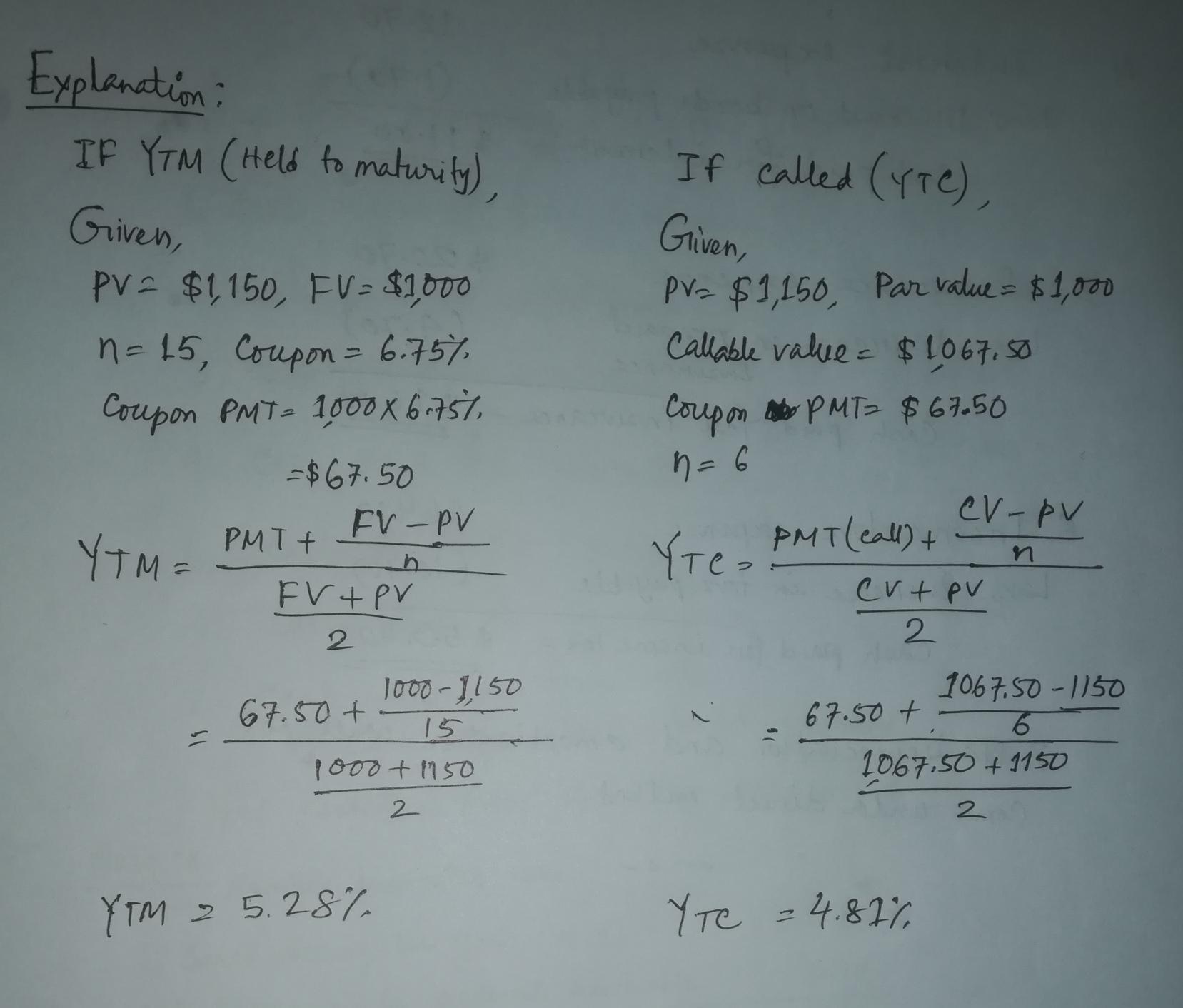

The rate of return should an investor expect to earn if he or she purchases these bonds is 4.81%

<h3>What is

rate of return?</h3>

A return in finance is a profit on an investment. It includes any change in the investment's value and/or cash flows received by the investor, such as interest payments, coupons, cash dividends, stock dividends, or the payoff from a derivative or structured product.

Annual Rate of Return: Definition and Calculation

For example, if an investment is worth $70 at the end of the year and was purchased for $60 at the start of the year, the annual rate of return is 16.66%.

A good return on investment is generally thought to be around 7% per year. Based on the historical average return of the S&P 500 after correcting for inflation, this is the barometer that many investors utilize.

(complete solution in attached image)

To know more about rate of return follow the link:

brainly.com/question/24301559

#SPJ4

Answer:

- <em>As explained below, given that the score of the person is among the 0.03125 fraction of the best applicants, </em><u><em>he can count on getting one of the jobs.</em></u>

<em></em>

Explanation:

The hint is to use <em>Chebyshev’s Theorem.</em>

Chebyshev’s Theorem applies to any data set, even if it is not bell-shaped.

Chebyshev’s Theorem states that at least 1−1/k² of the data lie within k standard deviations of the mean.

For this sample you have:

- mean: 60

- standard deviation: 6

- score: 84

The number of standard deviations that 84 is from the mean is:

- k = (score - mean) / standar deviation

- k = (84 - 60) / 6 = 24 / 6 = 4

Thus, the score of the person is 4 standard deviations above the mean.

How good is that?

Chebyshev’s Theorem states that at least 1−1/k² of the data lie within k standard deviations of the mean. For k = 4, that is:

- 1 - 1/4² = 1 - 1/16 = 0.9375

- That means that half of 1 - 0.9375 are above k = 4: 0.03125

- Then, 1 - 0.03125 are below k = 4: 0.96875

Since there are 70 positions and 1,000 aplicants, 70/1,000 = 0.07. The compnay should select the best 0.07 of the applicants.

Given that the score of the person is among the 0.03125 upper fraction of the applicants, this person can count of geting one of the jobs.

C. A resume is the correct answer