The purchase is based on the temporal effect and this comes under understanding the behavior of the consumer

Explanation:

Understanding the behavior of the consumer is also important because it depends upon each and individual consumer and the temporal effect includes at which time of the day the consumer is willing to take the item

Depending upon the climatic conditions the consumer can make his or her choice in this statement the purchase is made at the morning so the decision is made based on the temperature

Answer: False

Explanation:

Shoes and socks are complementary goods. A complementary good is a good that the demand for the good increases when there is reduction in price of its complement. Complementary goods have a negative cross elasticity of demand i.e. the demand for the good rises when the price of the other good decreases. Assuming "A" is a complement to "B" , a rise in the price of "A" will have a negative effect on the demand for "B".

A reduction in the price of A leads to a positive outcome on the demand for B resulting in an outward shift of its demand curve. The quantity demanded of one good has a direct relationship on the quantity demanded of the other good as they are linked together. When the price of shoes increases, less of socks will be demanded and vice versa.

I think the most appropriate answer would be D.

I hope it helped you!

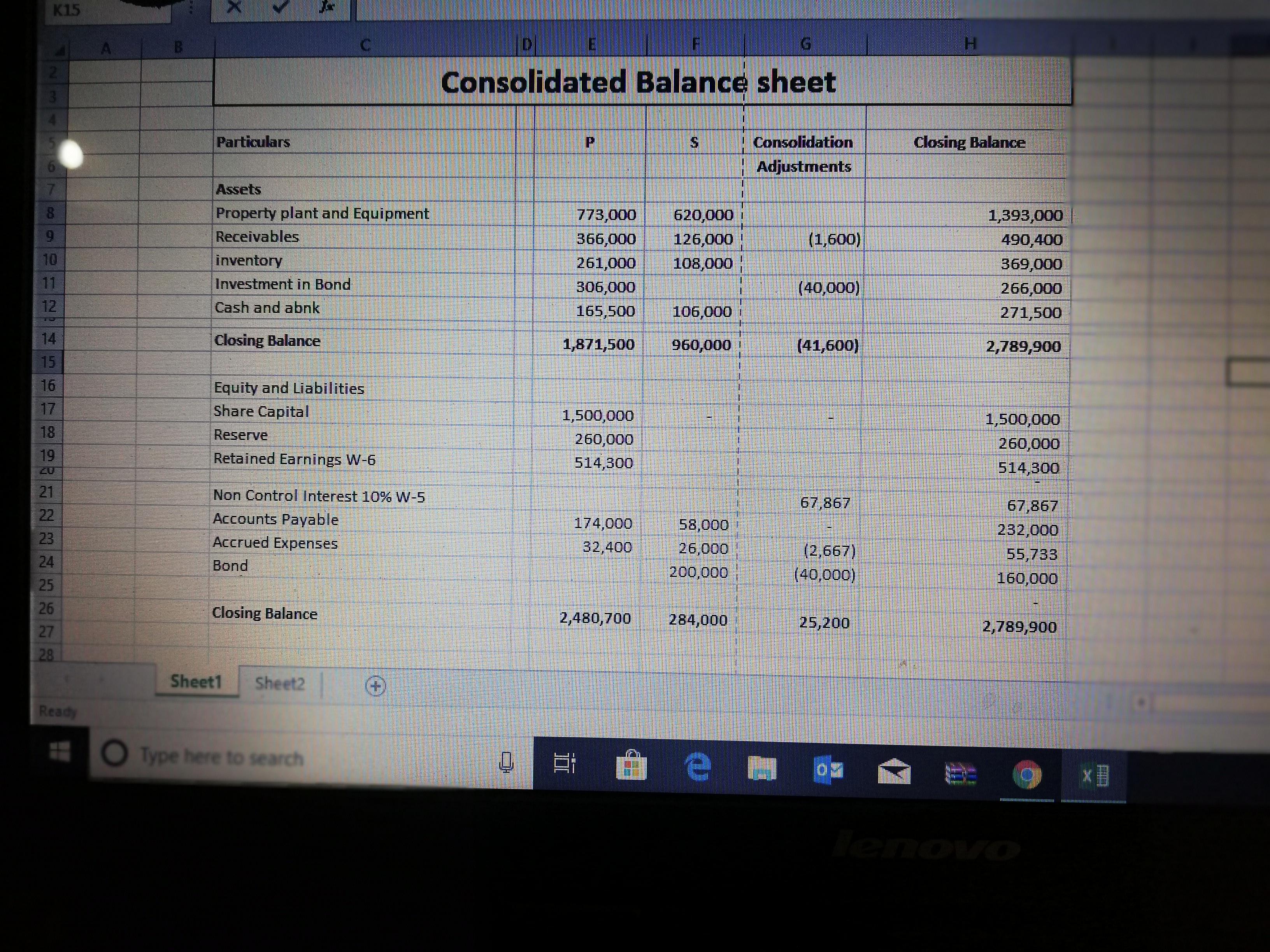

Answer and Explanation:

The computation is shown below;

For Alternative A

Cost to buy new machine -$119,000.00

Cash received $55,000.00

Reduction in variable manufacturing cost ($33400 - $23000) ×5 $52,000.00

Total change in net income -$12,000.00

For Alternative B

Cost to buy new machine -$112,000.00

Cash received $55,000.00

Reduction in variable manufacturing cost ($33400 - $10200) × 5 $116,000.00

Total change in net income $59,000.00

So here Xinhong should purchase a machine that belong from Alternative B.