Using the transportation method for solving the optimal shipping of a product from factories to warehouses is e) "≤" for constraints regarding factory capacity and "=" for constraints regarding demand at warehouses.

The transportation method of linear programming is applied to the problems associated with the examination of the efficient transportation routes i.e. how efficaciously the product from extraordinary sources of manufacturing is transported to exceptional locations, consisting of the overall transportation price is minimum.

The transportation model is a special class of linear programming that offers the delivery of a commodity from assets (e.g. factories) to destinations (e.g. warehouses) objective: The objective is to decide the transport agenda that minimizes the full transport price even as gratifying supply and call for limits.

The transportation method is a special case of linear programming issues wherein the goal is to limit the entire price of transporting items from diverse delivery origins to distinct demand destinations.

Disclaimer: The question is incomplete. Please read below to find the missing content.

Question: Using the transportation method for solving the optimal shipping of a product from factories to warehouses, as per text, you should use

a) "=" for constraints regarding factory capacity and "≥" for constraints regarding demand at warehouses

b) "≥" for constraints regarding factory capacity and "≤" for constraints regarding demand at warehouses

c) "≥" for constraints regarding factory capacity and "=" for constraints regarding demand at warehouses

d) None of the above

e) "≤" for constraints regarding factory capacity and "=" for constraints regarding demand at warehouses.

Learn more about transportation methods here brainly.com/question/13926750

#SPJ4

Answer:

B. $2,732,000.

Explanation:

After-tax operating income (ATI) = $3,200,000

Weighted-average cost of capital (WA) = 9%

Assets (A) = $7,000,000

Liabilities (L) = $1,800,000

Economic value added (EVA) is given by:

![EVA = ATI -[(A-L)*WA]\\EVA = \$3,200,000 - [(\$7,000,000-\$1,800,000)*0.09]\\EVA = \$2,732,000](https://tex.z-dn.net/?f=EVA%20%3D%20ATI%20-%5B%28A-L%29%2AWA%5D%5C%5CEVA%20%3D%20%5C%243%2C200%2C000%20-%20%5B%28%5C%247%2C000%2C000-%5C%241%2C800%2C000%29%2A0.09%5D%5C%5CEVA%20%3D%20%5C%242%2C732%2C000)

Endotrope's economic value added is $2,732,000

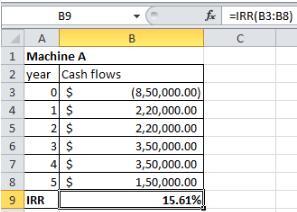

Answer:

The answer is "15.61%"

Explanation:

Please find the solution file in the attachment.

Answer:

D) $115,000

Explanation:

beginning 5,000 at cost of $ 35,000

purchase 12,000 at $9 each = $ 108,000

total units available for sale 17,000

ending <u> (4,000) </u>

sold units: 13,000

Under LIFO we first sale the newest units those are the purchased ones.

we will sale the 12,000 purchased unit --> $108,000

13,000 - 12,000 = 1,000 there is still 1000 more unit to sale oso we take themfrom beginning inventory

and 1000 of the beginning inventory:

35,000 / 5,000 x 1,000 = 7,000

total cogs = 108,000 +7,000 = 115,000

Answer:

the right to be informed. the right to be safe. the right to choose. the right to be heard. avenues for redress ofconsumer grievances (e.g., state and federal agencies, consumer protection laws, private groups such as Common Cause, Better Business Bureau).

Explanation:

A. being aware of the risks to consumer