Answer: the correct answer is A. Logistics and Supply Chain Management

Explanation:

Logistics and Supply Chain Management has to do with delivering and managing essential commodities, equipment, and services whether it is in an emergency or a routine operation in a company.

For low levels of output, aggregate supply curves are comparatively flat; for high levels of output, they are comparatively steep.

<h3>What is aggregate supply? </h3>

The total amount of merchandise that businesses will produce and sell is known as aggregate supply, or real GDP. The positive association between price level and real GDP in the short run is demonstrated by the upward-sloping aggregate supply curve, also known as the short run aggregate supply curve.

Price, time, employer remuneration, technical breakthroughs, inflation and deflation, governmental rules, and the availability of resources are some of the variables that influence the aggregate supply curves.

To know more about aggregate supply, visit:

brainly.com/question/29349235

#SPJ1

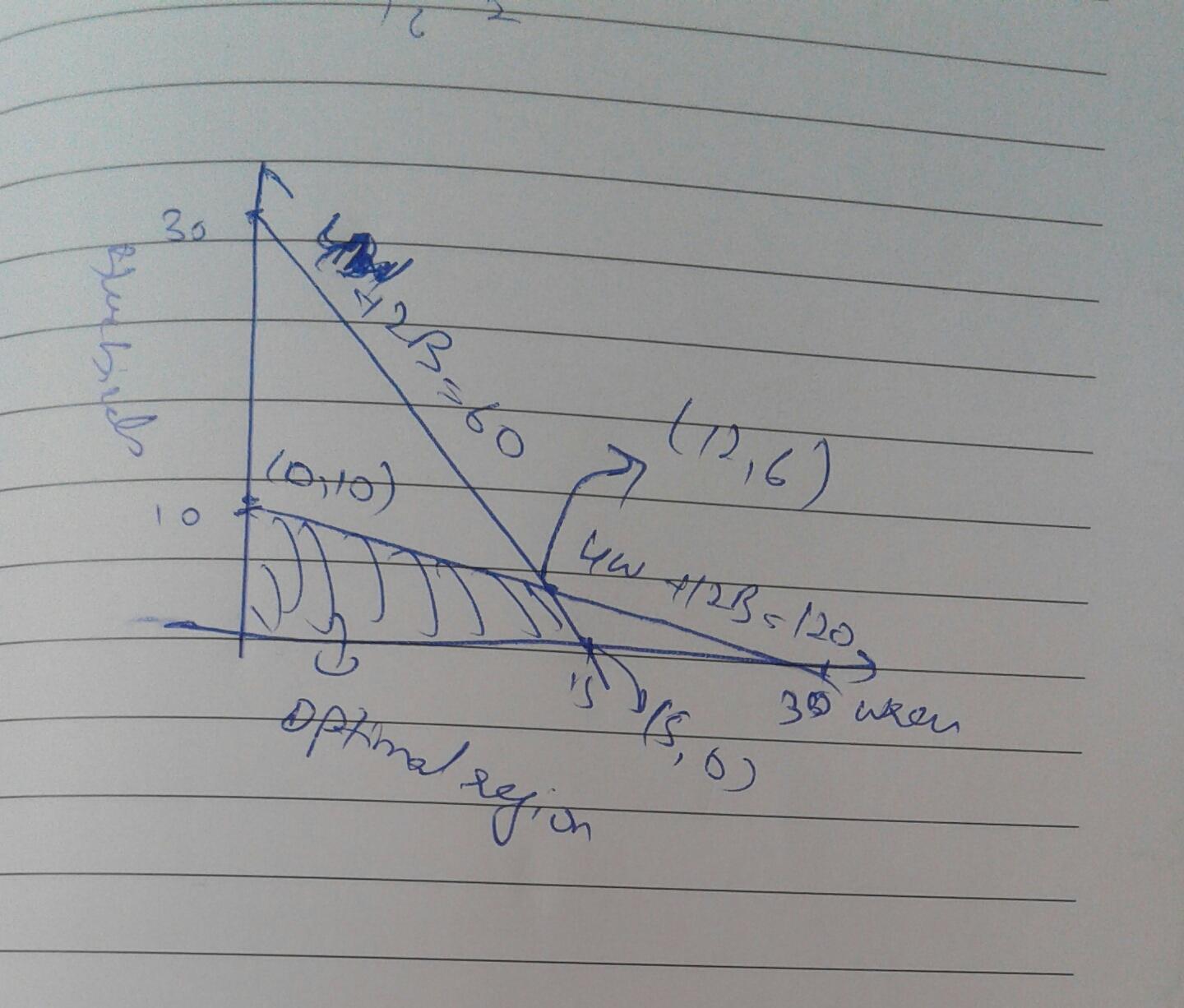

Answer:

a) 6W+15B

subject to:

4W+2B ≤ 60

4W + 12B≤ 120

W>0

B>0

b) see attachment

Explanation:

a) W: wren birdhouse

B: bluebird house

Objective function:

6W+15B

Explicit constraints:

4W+2B ≤ 60

4W + 12B≤ 120

Implicit constraints

W>0

B>0

b) coordinates of optimal region:

(0,0), (0,10), (12,6), (15,0)

For optimum profit:

(0,0): 6(0) + 15(0)= 0

(0,10): 6(0) + 15(10)= 150

(12,6): 6(12) + 15(6)= 162

(15,0): 6(15) + 15(0)= 90

Optimal solution is: (12,6) or 12 wren birdhouse and 6 bluebird house

Answer:

$38.0 millions

Explanation:

Cash paid to suppliers of merchandise = Cost of Goods Sold + Increase in inventory - Increase in accounts payable

Therefore, we have:

Cash paid to suppliers of merchandise = $40.0 millions + $4.5 millions - $6.5 millions = $38.0 millions