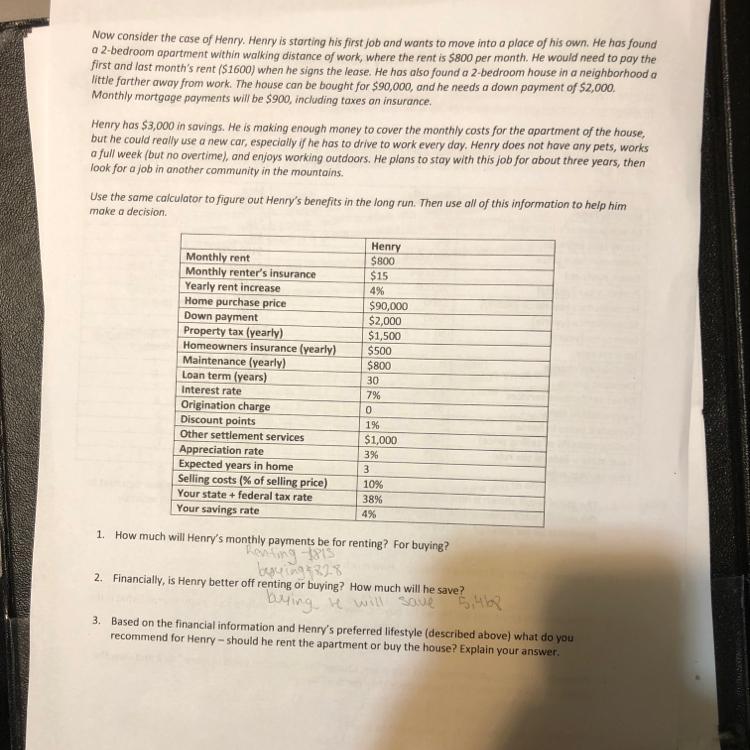

Answer:

Indirect materials $900 Favorable

Indirect labor $800 Unfavorable

Utilities $800 Unfavorable

Supervision $0 Neither Favorable Non Unfavorable

Total $700 Unfavorable

Explanation:

Preparation of a responsibility report for April for the cost center.

HANNON COMPANY Assembly Department Manufacturing Overhead Cost Responsibility Report For the Month Ended April 30, 2020

Controllable cost Budget Actual

Indirect materials $15,700- $14,800 =$900 Favorable

Indirect labor 21,300- 22,100 =$800 Unfavorable

Utilities 11,100- 11,900=$800 Unfavorable

Supervision 5,100- 5,100= $0 Neither Favorable Non Unfavorable

Total $53,200-$53,900=$700 Unfavorable

Therefore The responsibility report for April for the cost center will be :

Indirect materials $900 Favorable

Indirect labor $800 Unfavorable

Utilities $800 Unfavorable

Supervision Neither Favorable Non Unfavorable

Total $700 Unfavorable