Answer:

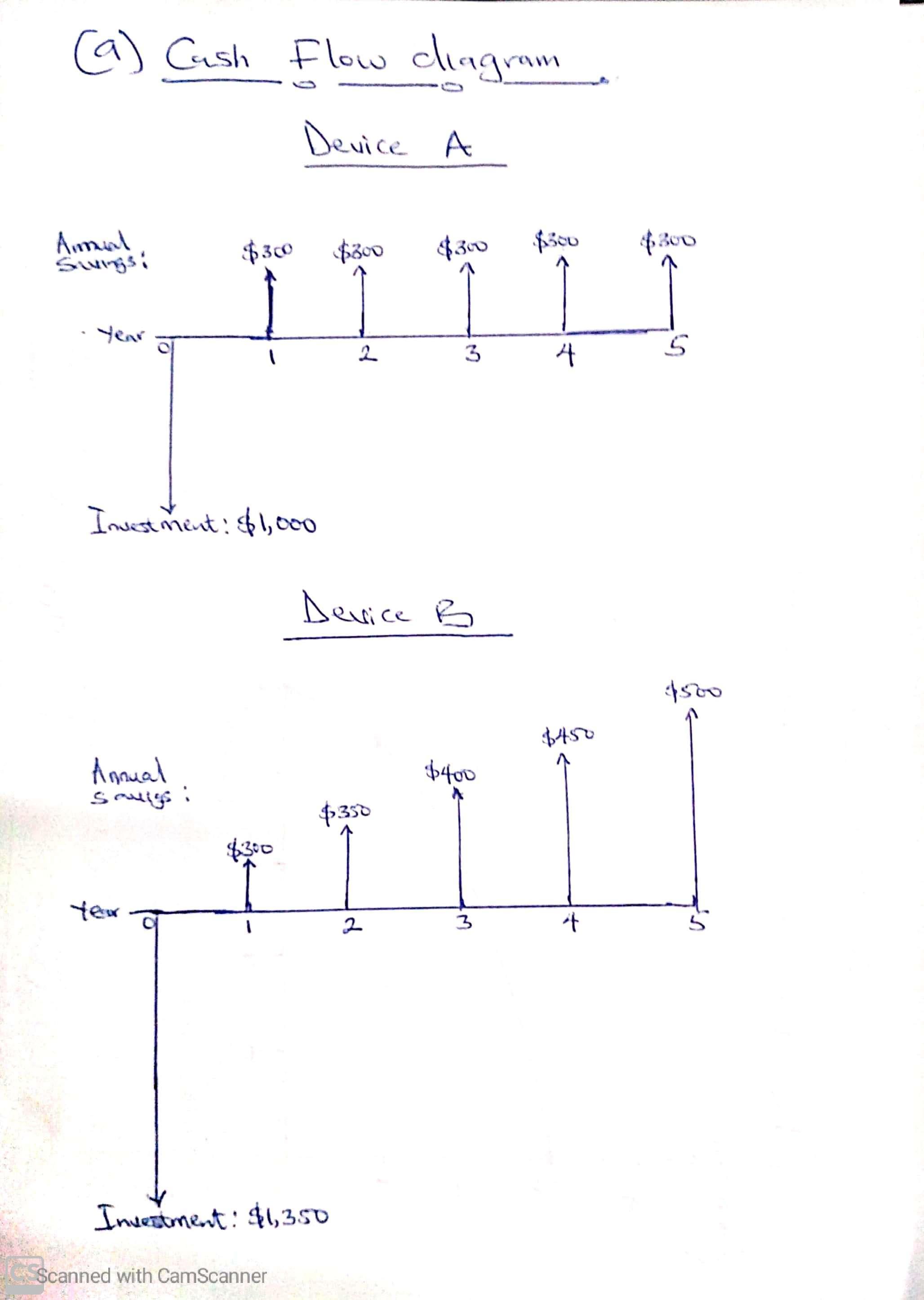

a) Find the attached jpeg file for the cash flow diagram

b) The company should purchase Device B.

Explanation:

a) Draw cash flow diagram for each option

A project cash flow diagram is a tool that is used to present a visual representation of the cost of a project and cash it is expected to generate over a specified period of time. On the diagram, x-axis represents the year, and y-axis represents cash out flows and/or inflows.

Note: See the attached jpeg for the cash flow diagram.

b) If interest rate is 7%, which device should your company purchase?

To determine this, we compare the Net Present Value (NPV) of the 2 devices.

Note: See the attached excel file for the calculation of the NPVs of the two devices.

From the attached excel file, we have:

NPV of Device A = $230

NPV of Device B = $262

Decision: Since $262 NPV of Device B is greater than the $230 NPV of Device A, <u>the company should purchase Device B.</u>

The project manager who is linked directly to the customer interface, and provides direction, coordination, and integration to the project team in project management.

Project managers (PMs) are responsible for planning, organizing, coordinating, integrating, and directing the completion of specific projects for an organization and ensuring whether these projects are on time and within budget.

The project manager should understand the scope of the project to be worked on and should estimate the time and resources required to fully deliver the targets to be reached for the project.

He also has to provide management procedures like managing time and structuring work to be done before the deadline.

The project manager holding the position as the head also serves as the team’s channel to higher management needs and challenges.

He should also resolve obstacles and blockers that may affect the team from doing the proper job and he should ensure that the team is focused on delivering the project objectives assigned as efficiently to present before the given deadline.

Learn to know more about the steps involved in protecting the team from distractions and resolving conflict between team members in project management on

brainly.com/question/27599974

#SPJ4

Is to collect information

Answer:

Investments in liquid securities, such as stocks, bonds, and derivatives, are not included in cash and equivalents.

Explanation:

Even though such things may be easily turned into cash typically with a three day settlement period, they are still excluded. The assets are listed as investments on the balance sheet.