Answer and Explanation:

1.

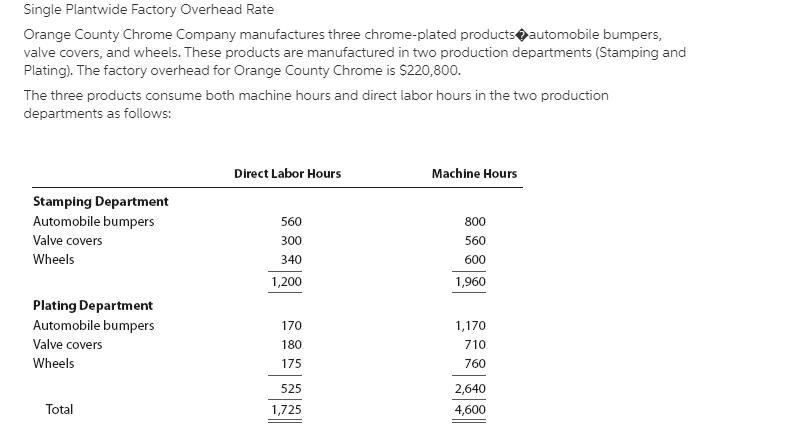

The direct labor overhead rate using the direct labor hours is shown below:-

Direct labor overhead rate = Total overheads ÷ Direct labor hours

= $220,800 ÷ 1,725

= $128

b. The machine hour overhead rate using the machine hours is

= Total overhead ÷ Machine hours

= $220,800 ÷ 4,600

= $48

2.

The factory overhead costs using direct labor hour is

Particulars Automobile Valve Wheels Total

bumpers covers

Direct labor

hours 730 480 515

Overhead rate $128 $128 $128

Total $ 93,440 $61,440 $65,920 $220,800

For determining the total overhead we simply multiply the direct labor hours with overhead rate.

The factory overhead costs using machine hour is

Particulars Automobile Valve Wheels Total

bumpers covers

Machine hours 1,970 1,270 1,360

Overhead rate $48 $48 $48

Total overhead $94,560 $60,960 $65,280 $220,800

For determining the total overhead we simply multiply the machine hours with overhead rate.