<span>By offering the customer a choice of more than one option that will satisfy their needs, Matt is using the "multiple options" sales closing method.</span>

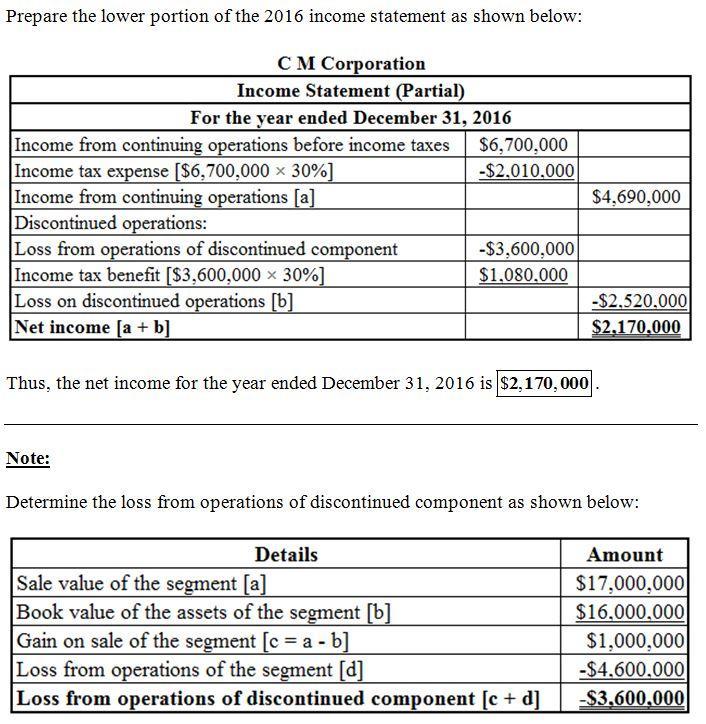

Answer

Net income = 2.170.000

Loss from operations of discountinued component = -3.600.000

The answer and procedures of the exercise are attached in a microsoft excel document.

Explanation

Please consider the data provided by the exercise. If you have any question please write me back. All the exercises are solved in a single sheet with the formulas indications.

Answer:

Business plan necessary because:

•It make you aware of your strength or weakness.

•It also creates an effective strategy for growth.

•It helps to determine your future financial needs.

•It also helps to gain a deep understanding of your market.

Answer:

The correct answer is letter "D": support of middle managers.

Explanation:

The Human Resources (HR) department is in charge of the recruitment process in every organization. Though there might be some limits at the moment of selecting new personnel such as the resources of the company, if the job offered is attractive enough or not, and if the company has a good reputation that attracts qualified labor hand.

<em>Middle managers do not represent a major constraint at the moment of recruiting new employees. In most cases, they are the ones requesting for more workers in their departments.</em>

The Cambridge's gross profit from this sale was $ 60,000.

<h3>

What is gross profit?</h3>

Gross profit is the amount a business makes after deducting the expenses associated with manufacturing and marketing its products or providing its services. Gross profit, which appears on an organization's income statement, can be calculated by subtracting the cost of goods sold (COGS) from revenue. An organization's income statement will contain numbers. Other of names for the gross profit include sales profit and gross income. Generally speaking, fixed costs are not included in gross profit (that is, costs that must be paid regardless of the level of output). Rent, advertising, insurance, salaries for staff not involved in the production directly, and office supplies are some examples of fixed costs.

To learn more about gross profit, visit:

brainly.com/question/14988657

#SPJ4