The answer is B. Blueprints for a house. Hope it help

Answer:

We can say the rate is close enought to 14%

Explanation:

tthe IRR will be the rate at wich the NPV is zero

The cash flow are an annuity of 4,120 for 6 years

NPV = present value of cash flow - investment

0 = PV of annuity - investment

0 = PV of annuity - 16,000

PV = 16,000

C 4120

time 6

rate IRR

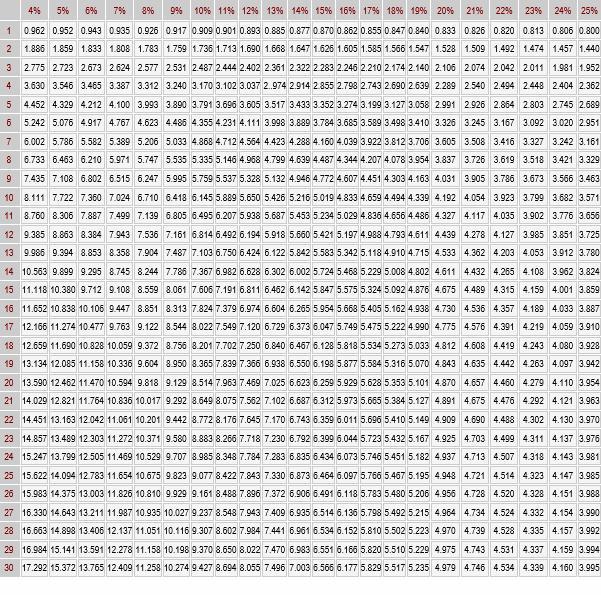

We divide the PV by the annuity to get the annuity factor

16,000 / 4,120 = 3,88349

We can look into the annuity table for a factor at time = 6 close to this figure

we have

14% factor of 3.889

15% factor of 3.784

We can say the rate is close enought to 14%

Answer:

a.varies a great deal across countries.

Explanation:

- Corporate governance is a mixture of the rules and laws by which the business operates and is regulated and controlled this term involves the external and the external factors that impact the compactors stakeholders, customers, shareholders, and the management.

- However the structure differs form nations to nations on the basis for the roles played by the governments and that includes the monitoring the actions, policies, and the decisions of the corporations.

- <u>Countries like the U.K, Canada, Ireland, United States, and New Zealand are the top five countries in the corporate governance scale with an overall rating of 7.6 to 6.7.</u>

Answer:

Price will increase by $277.58

Explanation:

Market rate of Interest of a zero coupon bond can be determined by following formula

Market Rate of Interest = [ ( F / P )^(1/30) ] - 1

4.25% = [ ( $5000 / P )^(1/30) ] - 1

0.0425 + 1 = ( $5000 / P )^1/30

( 1.0425 )^30 = (( $5000 / P )^1/30)^30

3.4856 = $5000 / P

P = $5,000 / 3.4856

P = $1,434.46

Now Calculate the change in Price

Change in price = $1,434.46 - $1,156.88 = $277.58

Price will increase by $277.58

propertyIsEnumerable() The propertyIsEnumerable() method returns a Boolean telling if the specific property is enumerable and is the object's own property.

Enumerable properties are those with an internal enumerable flag set to true, which is the default for properties created through simple assignment or a property initializer. Object-defined properties, such as defineProperty, are not enumerable by default.

We must use the Object. defineProperty() method to create a non-enumerable property. This is a special method for creating objects with non-enumerable properties.

Learn more on enumerable-

brainly.com/question/13068603

#SPJ4